IQ

Insight

Quarterly

Q2 | 2026

The used market: broadly recovered ahead of seasonal averages

Overall, the UK used car market is performing well, especially after a softer Q1. Q2 has broadly recovered ahead of seasonal averages, with values holding up well and retail demand remaining consistent. Clean, retail-ready stock is in the highest demand, while anything below that standard is facing resistance, both wholesale and retail.

These results were delivered against a challenging backdrop. Market conditions in the first half of 2026 were far from favourable, but not insurmountable. Retailers who moved quickly, responding to shifting market dynamics and proactively controlling stock mix and quality, weathered the storm; those who didn't are managing the consequences now.

What has become clear this year is that procurement discipline, especially for young electric vehicle (EV) stock, needs to be hardwired into retailers' buying strategies rather than applied reactively. AI-assisted appraisal and live pricing tools are becoming an operational necessity here: the ability to make faster, better-informed decisions at the point of sale is where the biggest margin gains are being won.

Residual values

While used vehicle values ran ahead of seasonal averages throughout Q2, EVs' historically weak performance has shown little improvement. Wholesale EVs aged two to four years are still trading at 32% of their original new cost, compared with 52% for petrol vehicles of the same age. This 20-percentage-point gap has shown little sustained convergence in recent years, with only marginal gains coming from a slight softening in petrol values.

It's important to recognise that while EVs are down as a fuel type overall, the picture looks very different model by model. Demand in some categories is now outpacing supply, a notable turn from earlier in the year, and values are rising for the right models at the right price points. But for every model up, another is still declining, which means model-level precision, not fuel-type averages, is now essential to understanding EV exposure and managing risk.

This quarter did see a genuine uptick in demand for used EVs, with interest in electric models up 36.4% in May on Autotrader. Confidence in the trend's staying power is weak, however: the surge was driven by an initial reaction to fuel-shortage headlines, and those headlines have since dropped out of the news cycle.

Future considerations

Today, the opportunity is clean, retail-ready stock. It's converting well and generating strong returns for retailers who can get hold of it. But that strong performance is itself the problem: clean stock is becoming a scarcer asset, and the premium on Grade one to three stock is hardening even as overall supply remains elevated. New car retail is generating higher volumes of older, lower-quality part-exchanges that are harder to price and turn.

The overall dynamics of the UK used car market are positive, with healthy demand and adequate stock supply. But the market is close to a turning point, beyond which the picture may look very different. Substantial volumes are set to enter the market in the second half of the year, and early signs are already visible across the industry. Pre-registration and demonstrator volumes are rising alongside fleet returns, leasing defleets and part-exchanges, driving up volumes in both retail and wholesale channels simultaneously. Combined with heavy discounting from new market entrants, this is putting real pressure on nearly-new values.

From here, the forward curve is clear. Used values are forecast to turn unfavourable against seasonal norms from Q4 2026, worsening through most of 2027 as volumes continue to rise. The overall premium versus pre-pandemic norms narrows from 27.9% today to 23.8% by mid-2027.

So, what should businesses do to prepare? In this environment, margin protection will depend on disciplined procurement, tight stock-ageing control, and careful management of exposure to young EV supply. Businesses still acquiring stock at elevated levels should stress-test that exposure now, before these conditions arrive.

It's also worth recognising that the channel you operate in is increasingly determining your margin outcome. Car supermarkets, for example, are turning stock significantly faster than independents. Operators without a clear, deliberate position on stock profile and pricing strategy will find themselves squeezed from both ends.

What's one key dynamic the industry needs to watch this year?

"The market should be watching closely for the convergence of rising used EV volumes and new-market-entrant stock entering the market at the same time. With no historic precedent to draw on, this combination could create a fragmentation challenge the market isn't yet calibrated for."

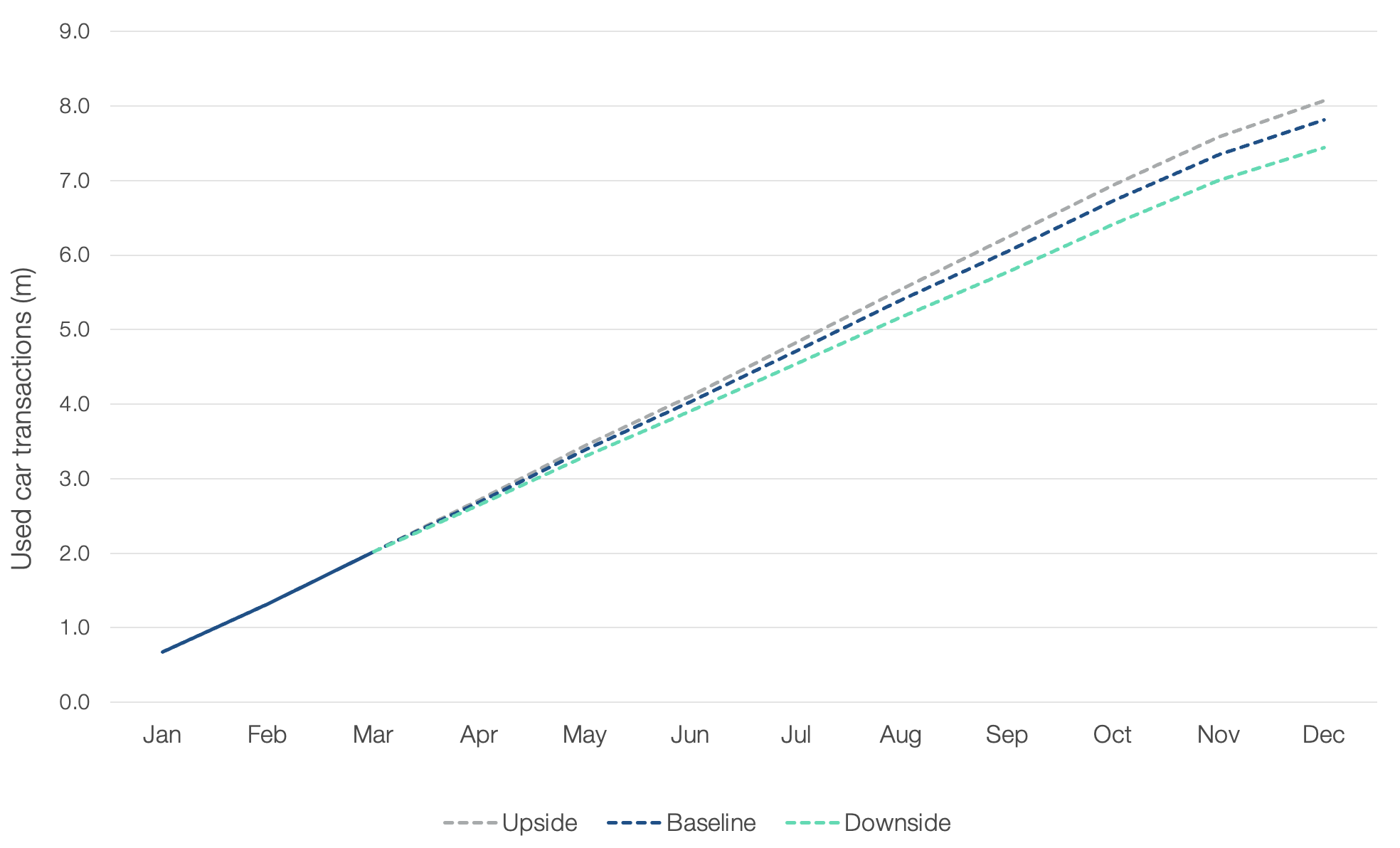

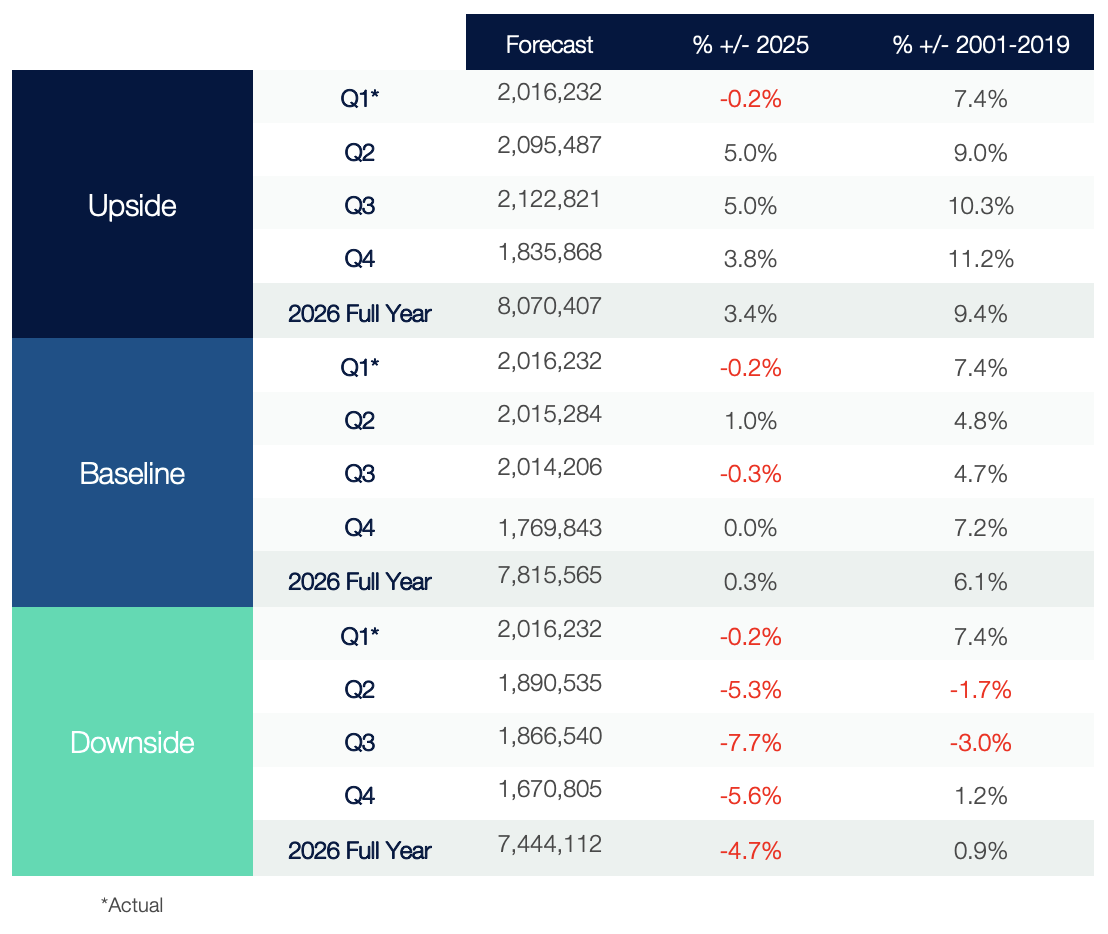

Used car forecasts

Each quarter, we integrate our proprietary market insight with the latest used-vehicle transaction data to produce three 12-month outlooks: upside, baseline and downside. These scenarios reflect differing macroeconomic, policy and industry assumptions, providing a structured framework to support stakeholder planning for potential developments in the used-car market over the year ahead.

The used market recovered ahead of seasonal averages in Q2, with clean retail-ready stock converting well, and cost-of-living pressure pushing buyers toward used vehicles. But the market sits close to a turning point. Pre-reg, demonstrator, defleet, and part-exchange volumes are all building at once, and the forward curve already points to values becoming unfavourable relative to seasonal norms from Q4. This evolving risk weighs heavily on the forecasts for the remainder of the year, despite initial positive results.

Our baseline scenario remains the most likely outcome, forecasting volumes to reach 7,815,565, a 0.1% year-on-year increase, essentially a flat market. That volume sits 6% above the long-term 2001-2019 average, confirming used cars' growing structural role in an affordability-led market, even as growth itself stalls.

The upside scenario assumes demand and dealer confidence stay resilient enough to absorb the coming stock wave without values cracking. Under this scenario, volumes could rise to 8,070,407 units, a 3.4% increase on last year and 9.4% above the long-term average, taking the market back through 8 million for the first time since the pandemic. Conversely, the downside scenario sees affordability pressure and competitive new-car discounting erode demand further than expected, with volumes falling to 7,444,112, a 4.7% year-on-year decline. Notably, even in this downside case, it would still land 0.9% above the 2001-2019 average, underscoring just how structurally embedded used demand has become.

Used Car Transactions Forecast 2026

Source: Cox Automotive

Upside scenario

In the upside case, the used-car market remains a core profit and cash-generation engine for retailers, with confidence and demand strong enough to absorb the stock wave in the second half of the year, without destabilising values.

- Dealers continue to prioritise used cars as a key revenue stream, absorbing rising pre-reg, defleet, and part-exchange volumes without a correction in values.

- Consumer confidence holds up as the Bank of England moves toward rate cuts, easing affordability pressure and supporting demand across core segments.

- Demand for used EVs sustains beyond the early-year spike, narrowing the residual gap versus petrol rather than reverting.

- Grade one to three stock scarcity eases as retailers get ahead of procurement with AI-assisted appraisal and pricing tools, protecting margin without needing to chase volume.

- Values remain broadly stable, keeping the premium versus pre-pandemic norms close to current levels rather than narrowing to 23.8%.

Baseline scenario

In the baseline view, the used-car market remains broadly stable, but margins come under sustained pressure as retailers work harder to protect throughput against a rising tide of stock.

- Used volumes track close to current levels, with only marginal year-on-year movement as growth stalls.

- Pre-reg, demonstrator and defleet volumes build as expected, pressuring nearly new values in particular.

- The EV residual gap persists and wholesale EVs aged two to four years still trade at around 32% of original cost, versus 52% for petrol, with model-level variation doing the real work rather than any fuel-type-wide recovery.

- Cost-of-living pressures keep used-car demand resilient overall, but affordability, not choice, remains the primary driver of purchase decisions.

- Margin protection depends on procurement discipline and stock-ageing control. The channel makes a significant difference, with car supermarkets turning stock over faster than independents and further squeezing the gap.

Downside scenario

In the downside case, affordability pressures intensify, and the new-car market's heavy discounting pulls demand away from used cars, increasing volatility in pricing and margins.

- Heavy new-car discounting and entry-level offers accelerate the erosion of used-car sales into new, faster than the baseline assumes.

- Inflation re-emerges more forcefully than the Bank of England’s central case, keeping rates higher for longer and weakening both consumer and business confidence.

- The simultaneous convergence of rising used-EV volumes and new-entrant stock entering the market creates a fragmentation problem that the market has no precedent for managing.

- Days to sell extend and stockholding risk increases, particularly for below-standard stock that's already facing resistance.

- Dealer margins are squeezed hardest at the bottom end of the stock quality spectrum, with the premium on clean Grade one to three stock the only reliable protection left.

Used Car Transactions Forecast 2026

Source: Cox Automotive