IQ

Insight

Quarterly

Q2 | 2026

New car market: Results from the UK new car market show robust performance and rising demand in Q2 2026

Headline results from the UK new car market show robust performance and rising demand. According to data from the Society of Motor Manufacturers and Traders (SMMT), over 523,000 cars were registered in Q2, a 13.3% increase on the same period in 2025. June alone outperformed the previous year by 11.4%. The picture is similar across Europe, up 5% year-to-date and forecast at 1.1% growth for the full year. But look beneath the headline, and this recovery is heavily incentive-led and offer-driven, still buoyed by fleet registrations.

Fuelling this growth is mounting competition from new market entrants, who are now battling not only established manufacturers but one another. The UK market's 13.3% growth accounted for 61,358 additional vehicles registered. In the same period, ten of the UK's newest brands registered over 36,000 vehicles, accounting for 60% of that total growth.

While the UK vehicle parc has reached a record high, the market is under mounting pressure from port congestion, inland storage constraints, rising logistics costs and increasing inventory levels. Some new entrants are planning on the assumption that the UK could become a three-million-unit annual new car market — a figure never achieved in the country's history, and a long way from our 2026 forecast of 2.19 million units. This raises important questions about the long-term sustainability of current supply and market expectations.

Influence of global dynamics

To understand the UK new car market today, it helps to understand the global dynamics behind it. The situation in China remains a major driver of uncertainty and volatility across the global automotive industry. In 2025, global vehicle production reached 96.3 million units, the highest level since 2017. China alone produced 34.5 million vehicles, equivalent to 35.8% of global output and 42.6% of all passenger cars manufactured worldwide. Yet despite this scale, Chinese production is operating at only around 55% capacity utilisation, against a backdrop of relatively weak domestic consumer demand. This growing imbalance is intensifying competition among exporters, with significant implications for vehicle pricing and market dynamics globally.

With the US market still off-limits to Chinese brands, Europe remains the focus. Chinese imports into Europe continue to grow despite EU tariffs of up to 35.3%, while BEV imports grew 61% year-on-year. Tariffs have reshaped the margin equation but have done little to stem the flow.

Separately, the price of oil is still up 47% and freight rates up 41% since the Iran conflict began, while battery commodity costs continue to rise. These pressures compound across production, logistics and supplier networks, and will feed into transaction prices through the second half of the year.

These are not seasonal patterns; they are structural shifts, compounded by geopolitical shock. The Iran conflict has created a cost environment the market hasn't planned for, and Chinese market entry has crossed 10% share in Europe.

Future considerations

Disciplined stock, pricing and capital management are no longer optional in this environment. New car volumes are likely to remain incentive-led and fragile, and businesses planning around current momentum as a new baseline are carrying more risk than the headline growth suggests.

Manufacturers are already being forced to rethink pricing strategies and product portfolios in response to sustained new-entrant pressure. Accelerating dealer consolidation and cross-border vehicle movement are adding further complexity, and the downstream consequences for aftersales, parts availability and residual values are only beginning to materialise. AI-driven pricing and stock management tools are increasingly being deployed to navigate this kind of volatility; the businesses building that capability now will be better placed when the next disruption arrives.

Consumer demand remains fragile, and we’re seeing signs that it is deteriorating further. Petrol prices are up 35.8% year-on-year, and affordability and monthly payments are now the primary drivers of purchase decisions. The Bank of England is holding rates at 3.75% while it monitors second-round inflation effects, with the MPC signalling it stands ready to act further if required. Consumer confidence should improve once rates eventually come down, but that pivot isn't imminent.

Tactical channel activity is also building a near-new supply problem. Manufacturers are using daily rental and short-cycle channels to manage month-end pressure in an increasingly competitive market. The pipeline this creates, near-new stock entering wholesale on compressed timelines and at below-market cost bases, will put direct pressure on pre-reg and demonstrator values through H2. It's already visible in the data.

What's one key dynamic the industry needs to watch this year?

"Brand loyalty is definitely one to watch. Cox Automotive consumer research found that over a third of respondents had changed their preferred vehicle manufacturer in the last six months, rising to 52% among drivers under 34. Further research from Autotrader reinforces this, finding that just one in seven respondents now agree European origin is important to them — half the level who agreed in 2024. This level of competition is unprecedented. The brands that move quickly to address value perception will be those that capture — or retain — market share. Those that don't are set to lose out, and winning it back will be a far greater challenge."

What should the industry be keeping a close eye on this year?

The industry should be closely monitoring the ongoing impact of the Iran conflict on global supply chains and oil markets, which represents the most significant near‑term disruptor to cost stability. Sustained volatility in oil prices has direct implications not only for vehicle running costs and consumer demand, but also for manufacturing, logistics and dealer operating expenses.

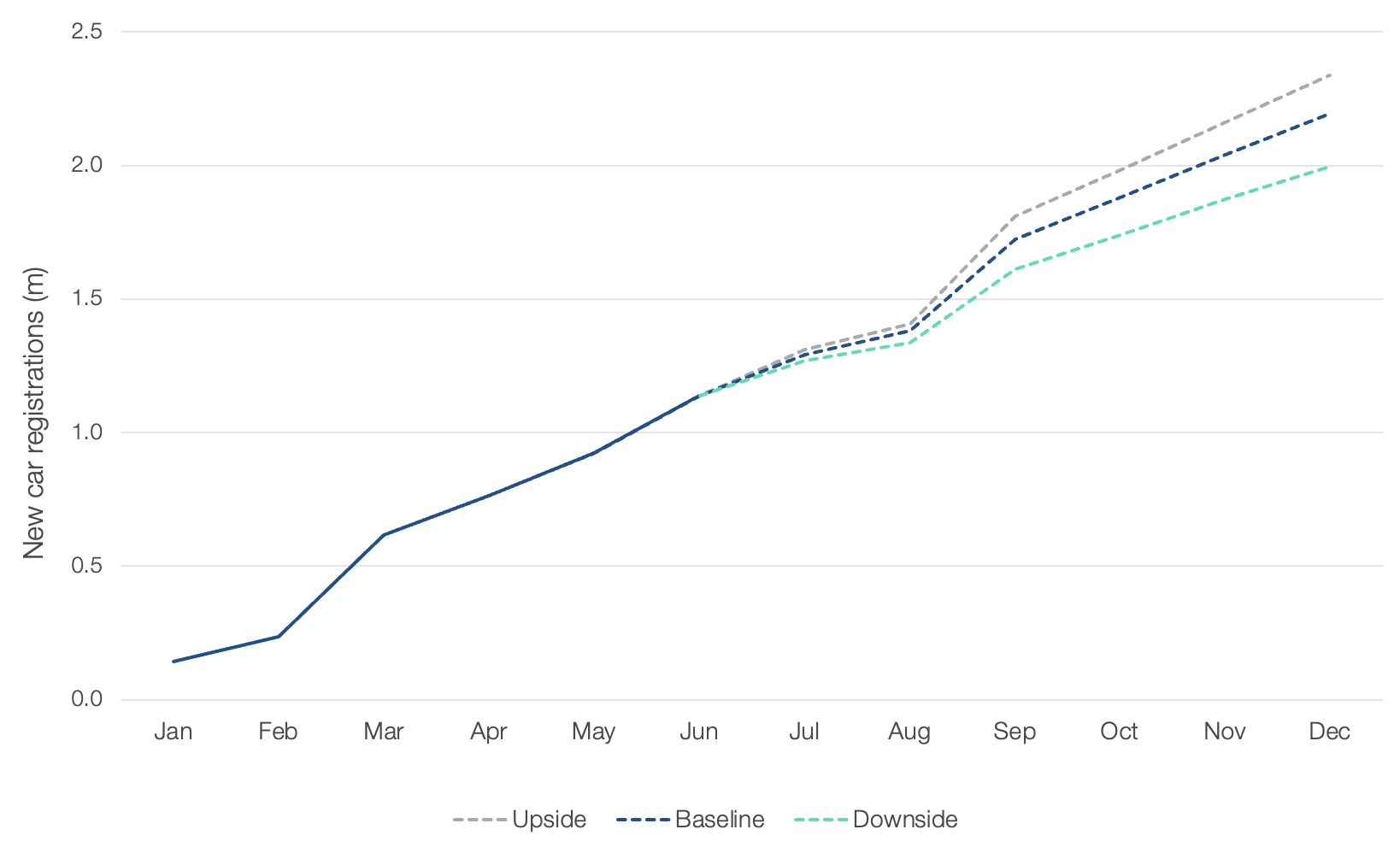

New car market forecasts

Each quarter, we integrate proprietary market insight with the latest registration data to produce three 12-month outlooks: upside, baseline and downside. These scenarios reflect differing macroeconomic, policy and industry assumptions, providing a structured framework to support stakeholder planning across a range of potential market outcomes.

This quarter's forecasts sit against a market that is growing on paper but fragile beneath the surface. Registrations are up, but the growth is incentive-led, fleet-heavy and increasingly propped up by new entrants rather than underlying demand. That growth is now colliding with three unforeseen dynamics. The Bank of England holding rates at 3.75% while it watches for second-round inflation effects, a change of Prime Minister mid-transition, with the ZEV Mandate's 2030 target under review, and an energy shock still working its way through fuel, freight and battery costs.

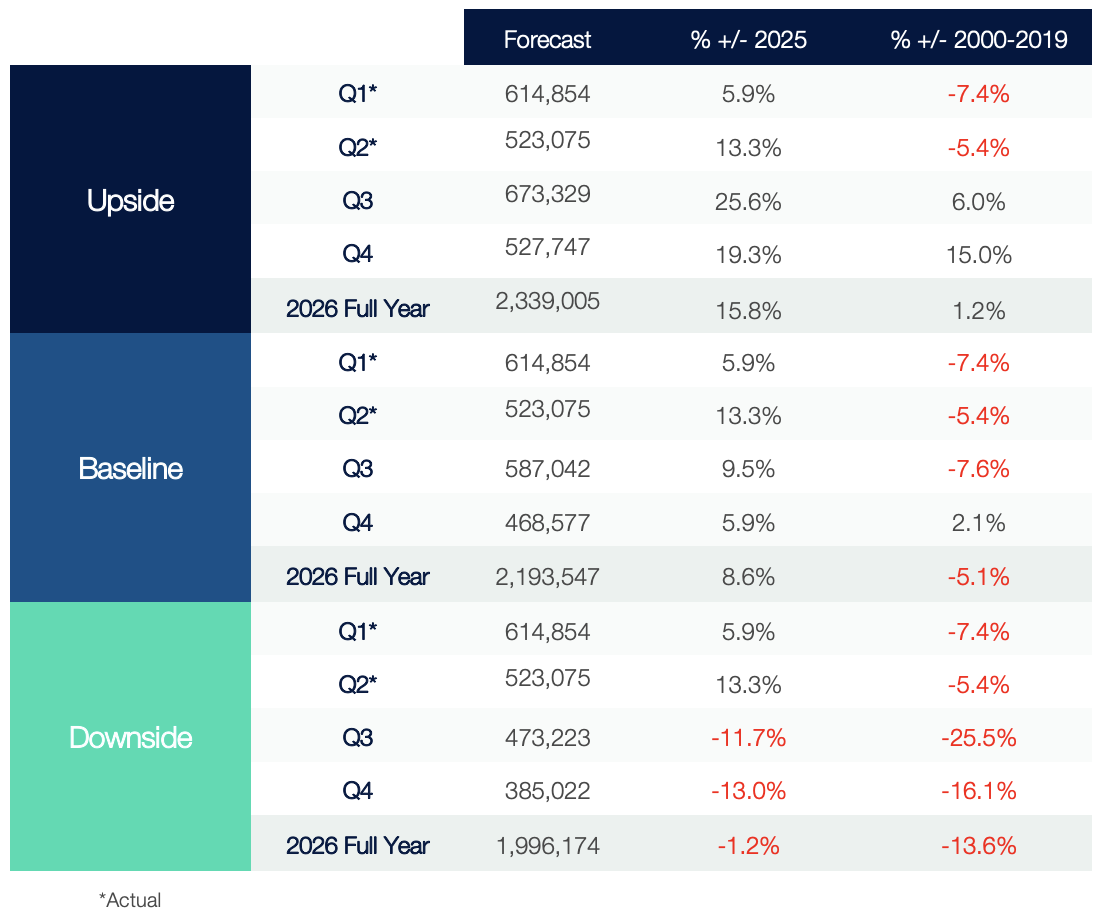

Our baseline scenario remains the most likely outcome, forecasting registrations to reach 2,193,547 units, an 8.6% year-on-year increase. Despite this growth, volumes would still sit 5.1% below the long-term 2000-2019 average, reinforcing that this recovery is manufactured rather than organic.

A more optimistic scenario, with rates easing and the ZEV Mandate review landing quickly and favourably, would see registrations rise to 2,339,005, a 15.8% increase on last year and 1.2% above the 2000-2019 average, the first time this decade the market would clear that bar. Conversely, the downside scenario anticipates political drift, a stalled mandate review and a further inflation shock combining to choke demand. This would see registrations fall to 1,996,174, a 1.2% year-on-year decline.

New Car Registrations Forecast 2026

Source: Cox Automotive

Upside scenario

In the upside case, the energy shock fades faster than expected, the new Prime Minister moves quickly to resolve uncertainty around the ZEV Mandate, and the Bank of England has room to cut interest rates. As a result, growth shifts from incentive-led to demand-led.

- The Middle East ceasefire holds, oil and freight costs normalise, and battery commodity pressure eases through the second half of the year.

- A new PM in place by September resolves ZEV Mandate uncertainty fast, with the 2030 target softened to something manufacturers can plan against rather than finesse their way out of.

- Inflation peaks below 3% and plateaus, giving the Bank of England room to cut from Q4. Consumer confidence lifts as borrowing costs fall.

- New entrants keep expanding the market rather than just cannibalising incumbent share, and affordability gains pull some used buyers back into new.

- Manufacturers ease off discount-led registration tactics as underlying demand firms up, reducing pressure on near-new and pre-reg values.

Baseline scenario

In the baseline view, the political and monetary backdrop stays unresolved for longer, but the market remains resilient enough to keep growing on the back of incentives and fleet activity.

- The energy shock persists into the second half of the year, keeping fuel and logistics costs elevated without triggering a sharp contraction in demand.

- The ZEV mandate review drags on through the leadership transition. Manufacturers keep managing to target via discounting and short-cycle channels rather than clarity.

- The Bank of England holds interest rates at 3.75% into Q4, with inflation persisting in the 3-3.5% range. Second-round wage effects stay contained but keep a cut off the table.

- Chinese manufacturers and other new entrants continue to gain market share, masking softer underlying demand through choice and competitive pricing.

- Near-new supply from daily rental and short-cycle channels continues to build, pressuring pre-reg and demonstrator values throughout the second half of the year.

Downside scenario

In the downside case, political uncertainty, a stalled mandate and deeper inflation combine to suppress demand and expose how fragile the current growth really is.

- A leadership transition that extends beyond September or produces a less industry-friendly outcome leaves manufacturers without clarity on ZEV mandate targets or fines.

- Energy prices spike again, inflation pushes towards 4%, and the Bank of England is forced to raise rates rather than cut.

- Consumer confidence stalls, ownership cycles extend, and affordability concerns dominate purchase decisions.

- Manufacturers lean harder on incentives and short-cycle registrations to hit volume, accelerating the near-new supply problem and dragging down residuals.

- New-entrant momentum slows as funding conditions tighten and margin pressure bites, removing one of the few genuine sources of market growth.

New Car Registrations Forecast 2026

Source: Cox Automotive