Welcome to the latest edition of Cox Automotive's Insight Quarterly, analysing the forces shaping the UK and European automotive markets in the second quarter of 2026.

As ever, this report combines data-led insight and market intelligence from across the new, used and electric vehicle sectors, helping to look beyond the headline numbers and understand the realities driving market performance.

At first glance, the second quarter presents a picture of strong momentum. New car registrations have continued to grow across the UK and Europe, electric vehicle adoption has accelerated and the used vehicle market has recovered well from a softer start to the year. On paper, these are encouraging results. Yet, as this quarter's analysis reveals, much of that growth remains highly dependent on incentives, tactical activity and competitive market intervention rather than a sustained strengthening of underlying consumer demand.

The new car market remains at the centre of this dynamic. Rising volumes are being fuelled not only by fleet demand, but increasingly by an unprecedented wave of competition from new market entrants. While this is providing consumers with greater choice and supporting registration growth, it is also creating significant pressure across pricing, supply chains and inventory management. At the same time, geopolitical developments, including ongoing disruption to energy and logistics markets, are increasing costs throughout the automotive ecosystem. Beneath the headline growth figures, questions around long-term sustainability, profitability and market capacity are becoming more difficult to ignore.

Meanwhile, the used vehicle market has demonstrated resilience, with demand for clean, retail-ready stock remaining strong and values performing ahead of seasonal expectations through much of the quarter. Yet here too the outlook is becoming more complex. Growing volumes of pre-registered vehicles, demonstrators, fleet returns and young EV stock are expected to enter the market over the coming months, creating new challenges for pricing, procurement and risk management. As supply continues to build, the ability to make fast, informed decisions on stock acquisition and valuation will become increasingly important.

Electric vehicles continue to be a major growth story. Higher fuel costs, evolving policy measures and substantial manufacturer incentives have all contributed to rising adoption rates across the UK and Europe. However, the sector remains at an important crossroads. Regulatory uncertainty, shifting government priorities and persistent challenges around residual values continue to complicate the transition. While the total cost of ownership case for EVs is becoming stronger, market confidence still relies heavily on policy clarity, infrastructure development and the industry's ability to communicate value effectively to consumers.

Taken together, the key message from this quarter is that growth alone no longer tells the full story. Across the automotive market, volatility is being shaped by a combination of geopolitical events, regulatory developments, technological change and intensifying competition. In this environment, success will depend on disciplined decision-making, effective use of data and the ability to adapt quickly as conditions evolve.

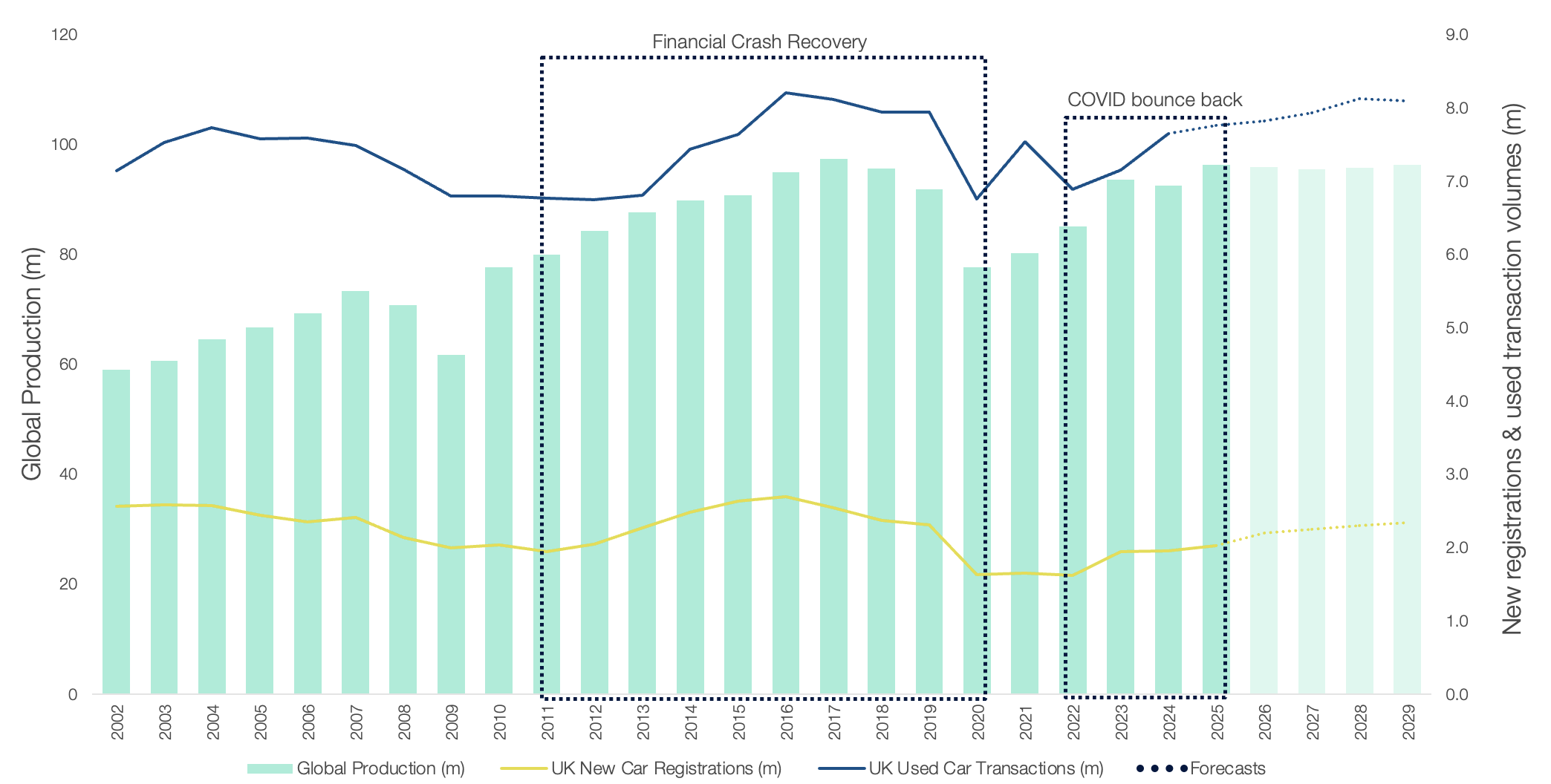

New & Used Sales vs. Global Production Volumes

Source: Cox Automotive