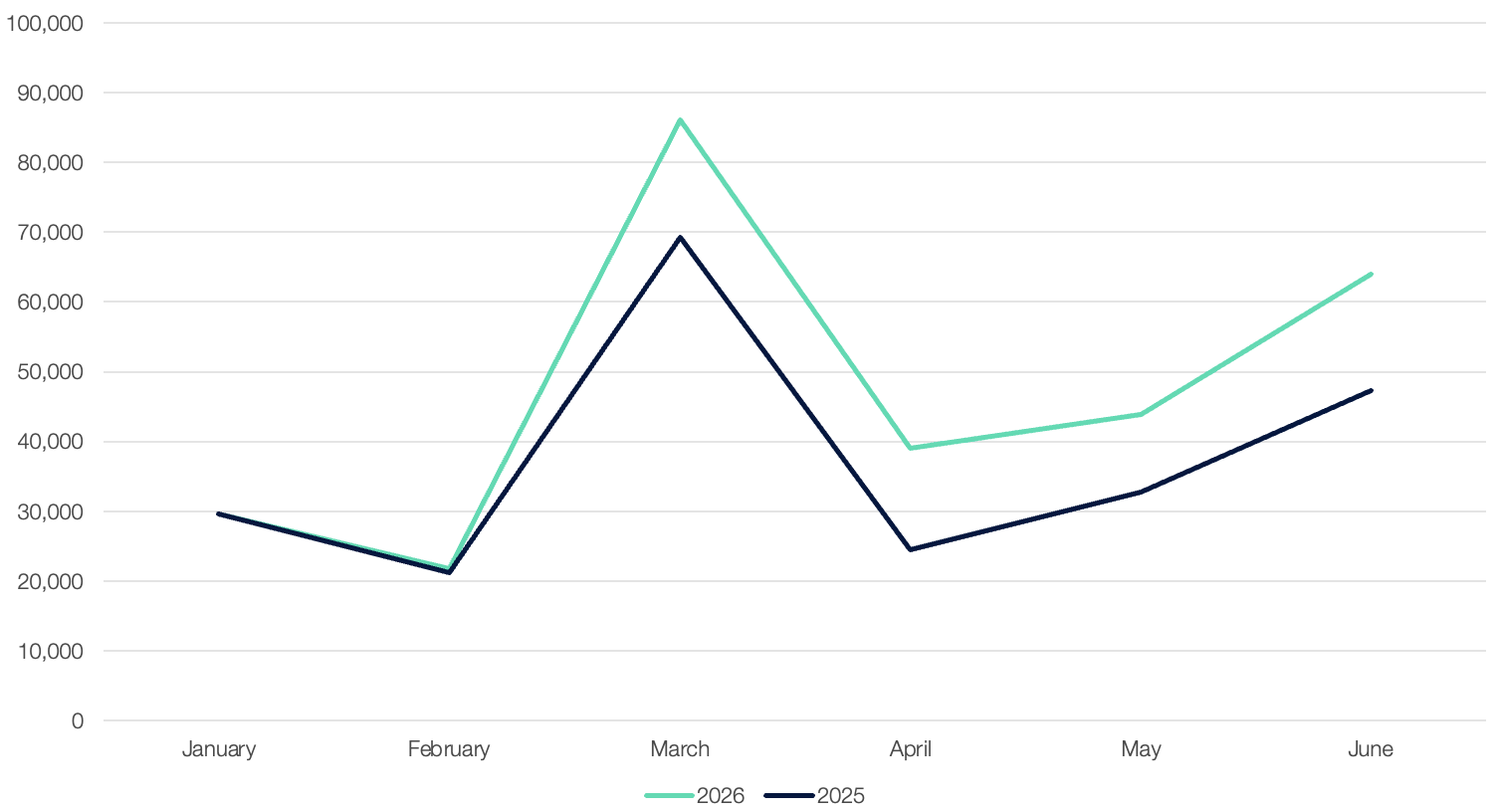

Electric vehicles (EVs) have, on the surface, had a successful year so far. In the UK, EV sales increased by 35% year-on-year, with EV market share reaching 30.0% in June. In Europe, EV sales have grown for 17 consecutive months, reaching 20% market share in May; year-on-year, sales in Germany were up 40.9%, France up 55.4% and Italy up 75.7%.

Most notable in the UK was the uptick in EV demand in March, following the outbreak of the Iran conflict and the fuel price pressure that followed. With fuel costs still up 35.8% in the UK, the running-cost comparison between petrol/diesel and electric ownership has tilted firmly in EVs' favour. This underlines that the case for electric transport is real and compelling, especially while fuel supply remains unstable — though whether it marks a lasting shift in consumer mindset is yet to be seen.

UK EV Registrations

Source: SMMT

EV results have been further bolstered by evolving policy dynamics. In the UK, manufacturers continue to manage the tension between compliance and commercial targets, leaning on hybrid vehicles and tactical registrations to meet ZEV mandate targets. In Europe, government subsidies are contributing significantly to EV adoption, with reintroduced and extended purchase grants across Germany, France and Italy directly driving Q2 volumes. These incentive structures are pulling the market forward, while organic consumer demand still lags behind.

Evolving regulation

There is a degree of uncertainty around the future of EV policy on both sides of the Channel. Following the European Commission's announcement in December of a proposed revision to the bloc's CO₂ emissions standards for cars and vans — from a 100% reduction target by 2035 to 90% — the UK is also facing a legal challenge over its current mandate targets.

Should targets be dialled back, as reports suggest, the impact would not be felt evenly. While it would offer the industry some much-needed relief amid a market already rocked by geopolitical and economic shocks, a revision would land hardest on those who've committed most to the transition. Manufacturers that have committed to electrification face stranded investment costs, while retailers and fleet operators that have structured their propositions around mandate-driven availability face the need to replan rapidly. Fleet customers may be among the most exposed: softening the mandate would directly extend dependency on petrol and diesel vehicles and undermine total-cost-of-ownership predictability across contract cycles.

It isn't just the ZEV mandate complicating the picture for the UK EV market. The Vehicle Excise and Trading Scheme (VETS) is expected to reduce car registrations from 2027, particularly for hybrids, and the introduction of the Electric Vehicle Excise Duty (E-VED) has been widely criticised as "the wrong measure at the wrong time." There is still no VAT harmonisation on public charging, and while the government has committed to reviewing public charging infrastructure, no timeline yet exists.

As it stands, the regulatory landscape is pulling in multiple directions. A review of current mandate targets is warranted, given the widening gap between regulatory ambition and market reality — but it needs to be carried out with proper consideration for the impact any softening will have on the wider market. Above all, the UK automotive industry needs certainty and confidence.

Future considerations

In the short term, the total cost of ownership and running-cost conversation is becoming easier to have with customers; fuel price pressure is doing some of the work. EV demand is forecast to keep growing, with independent retailers returning to the market.

Longer term, the challenge is more structural. Used EV values remain at a meaningful discount to ICE equivalents, an average of -15.8% penalty at 36 months, a marginal improvement from -17.9% earlier this year. However, new-car pricing from Chinese entrants continues to put pressure on younger used EVs.

AI-powered whole-life cost tools are emerging as a genuine customer-facing asset. The ability to model and present a compelling, personalised TCO case in real time is becoming a meaningful differentiator in EV retail conversations.

The total cost of ownership advantage is real; however, it doesn’t sell itself, and commodity costs are narrowing the margin for error. Battery raw material prices are rising across all key inputs, directly pressuring the delivered cost of new EVs and eroding the competitive advantage that has supported recent volume growth. The running-cost case for EVs remains compelling, but it needs active, evidence-based communication.

What's one key dynamic the industry needs to watch this year?

Chinese EV entrants are, at once, the biggest growth driver in new registrations, the biggest risk in used, and the most significant long-term disruptor to established EV brand premiums. However, these new-entrant EVs sit at approximately 45% future retail RV at 36 months, versus 66% for established brands. New-entrant EV pricing is setting a used-market floor that will reshape the entire segment. Chinese EV used stock is generating disproportionately high consumer interest relative to its current supply, an early signal of where buyer demand is concentrating.

As purchase barriers continue to fall and volume builds, pricing will increasingly anchor the floor of the wider used EV market, compressing residual values across the board. Understanding your exposure to this dynamic now, rather than when it arrives at scale, is where margin protection starts.