IQ

Insight

Quarterly

Q1 | 2026

The used market: supply and values remain under pressure

Home

Home

The New Market

The New Market

The EV Market

The EV Market

The restructuring ripple: How slow EV adoption is reshaping automotive value chains

The restructuring ripple: How slow EV adoption is reshaping automotive value chains

The missing generation: How the pandemic stock gap is reshaping the UK used car market

The missing generation: How the pandemic stock gap is reshaping the UK used car market

Automotive advertising: changing habits for big gains

Automotive advertising: changing habits for big gains

The minefield just got more dangerous

The minefield just got more dangerous

Appendix

Appendix

The used market continues to be a source of stability amidst ongoing turbulence. Despite geopolitical and regulatory uncertainty, the used market remains stable overall, however performance does vary significantly by fuel type and vehicle age. Rising wholesale volumes and steady conversion rates highlight healthy demand, especially as rising costs of living push drivers to delay new purchases and consider lower priced, used alternatives.

Low levels of car production in Europe (-3% year-on-year forecast for Q1 2026) is constraining the flow of some key quality used stock to the UK, while we are seeing growing stock levels for young electric vehicles (EVs).

While the market does usually see vehicle supply tighten following Q1, the shortages we are seeing in the market today are more structural than seasonal, driven largely by this multi-year new car under production, especially for petrol and diesel vehicles.

Residual values

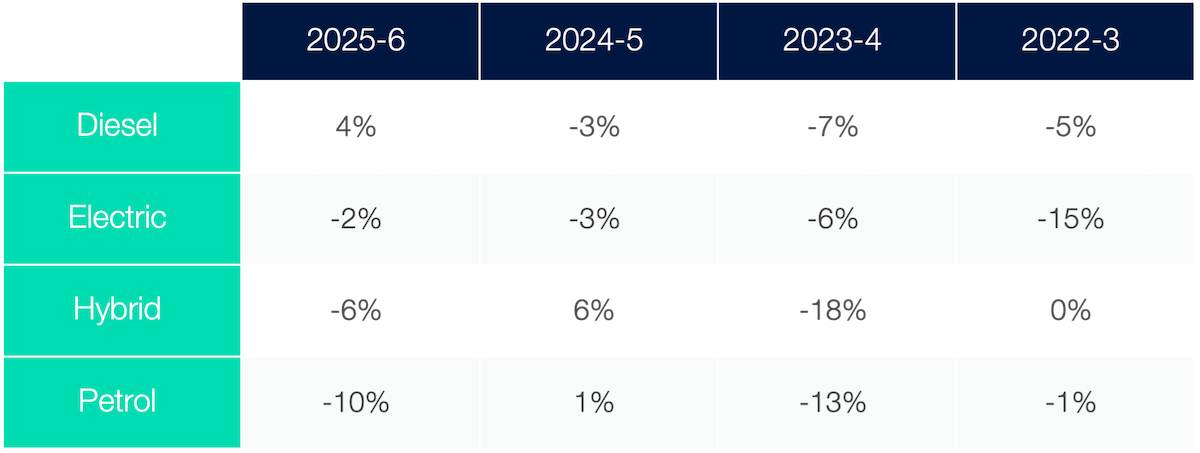

Looking at depreciation trends over time, it is easy to become absorbed in the overall decline over the past five years. Overall, used values have dropped since the highs of the pandemic took vehicles under 12 months selling at over 90% in some cases. However, rather than a negative signal, this may point to market correction, as we return to more stable depreciation rates. Looking at the earliest data available pre-pandemic, between January and March 2020, vehicles under 12 months were selling for an average of 65% of original cost new, the same as the current average for the same period in 2026.

While many factors still exert pressure on the rate of depreciation, the speed at which values have declined has slowed significantly in the last several years. Comparing year-on-year residual value data for vehicles between one to two years-old from March between 2023 and 2026, the most rapid pace of depreciation was seen between 2023 and 2024, with double-digit depreciation on average across all fuel types, values then held firm between 2024 and 2025.

Used Car Depreciation By Fuel Type

Source: Cox Automotive

While the overall rate of depreciation is slowing, we are still seeing some sharp drops in values in the nearly new petrol market. Values for petrol vehicles under 12 months old dropped to the lowest rate seen since the start of 2022 in December (62%), down 12 percentage points from the beginning of the year. While they climbed back up in January and February 2026 (71% and 77% respectively), we have seen another sharp drop to 65% in March. A mix of weakened demand with oversupply have led to a significant drop in values, especially as we are seeing high volumes of petrol from lease companies entering the used market.

Future considerations

Looking ahead, the outlook for the used market remains mixed, shaped by both short‑term cost pressures and longer‑term structural change. In the near term, higher stock acquisition costs may persist as competition for limited supply remains strong in certain segments. However, this environment may also support healthier margins on fuel‑efficient and hybrid vehicles, where demand remains resilient and consumer focus on running costs continues to intensify.

At the same time, shifts in consumer demand are becoming more pronounced. Volatility in fuel prices, taxation and ownership costs continues to influence purchasing behaviour, with buyers placing greater emphasis on total cost of ownership rather than outright purchase price alone. This is likely to benefit vehicles that offer predictable and efficient running costs, while demand for less economical models may remain more fragile.

What should the industry be keeping a close eye on this year?

The pace of Chinese vehicle imports into Europe is a key area of focus. Growing volumes of competitively priced Chinese‑manufactured EVs are increasing overall supply across European markets, with potential knock‑on effects for pricing dynamics throughout the used EV landscape.

As new EV supply expands, particularly at the more affordable end of the market, there is likely to be further pressure on used EV residual values. This may be felt most acutely among younger used stock, where pricing gaps between new and used vehicles are already under scrutiny. If supply continues to build at pace, maintaining value stability may become increasingly challenging without sustained growth in consumer demand. Understanding how new supply influences used pricing trajectories will be critical to managing risk, informing procurement strategies and setting realistic residual value expectations as the market continues to evolve.

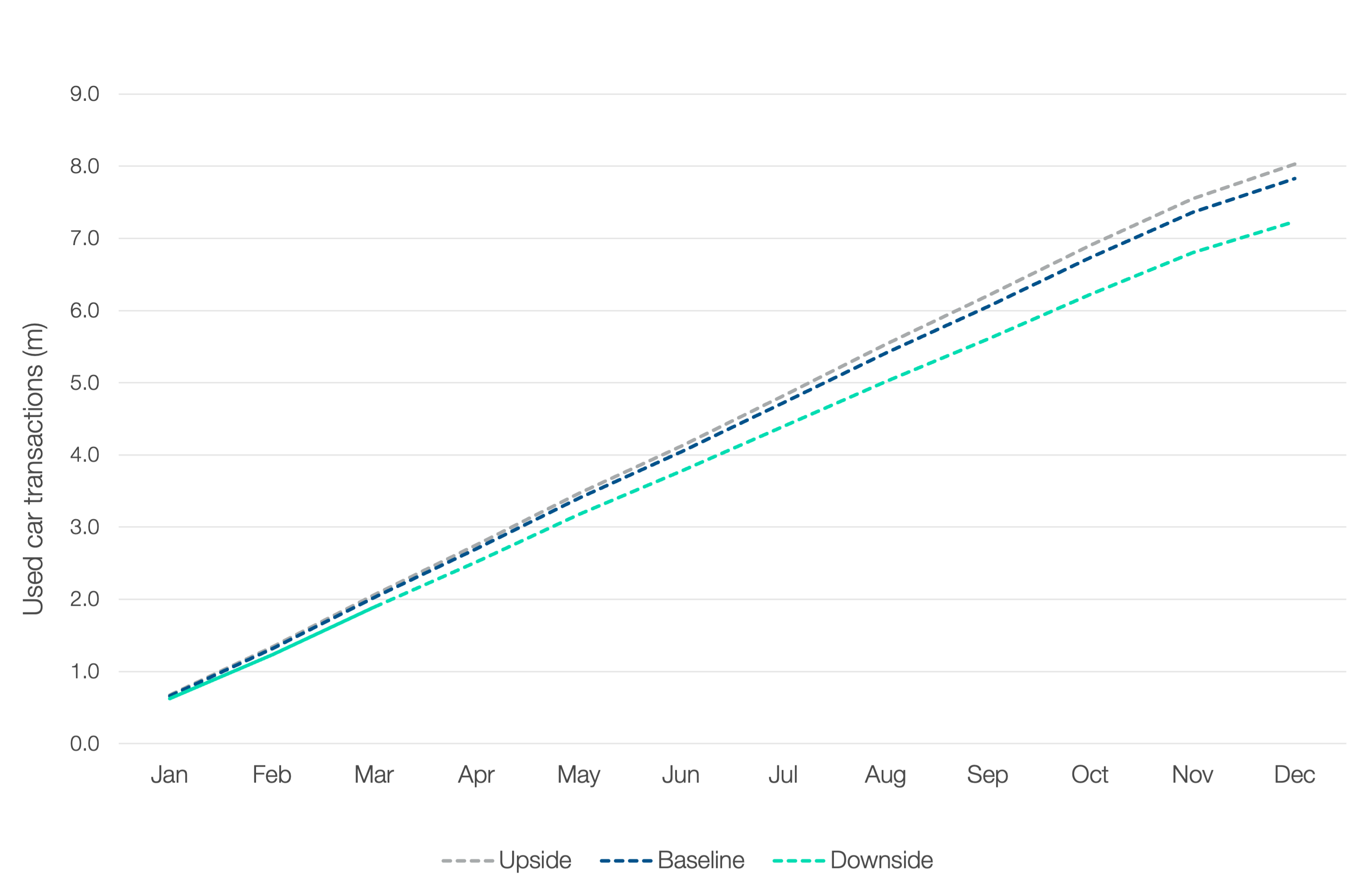

Used car forecasts

Each quarter, we integrate our proprietary market insight with the latest used-vehicle transaction data to produce three 12-month outlooks: upside, baseline and downside. These scenarios reflect differing macroeconomic, policy and industry assumptions, providing a structured framework to support stakeholder planning for potential developments in the used-car market over the year ahead.

In our most likely scenario, the baseline forecasts show relative stability in the market. Volumes are expected to reach 7,827,658 units, which would represent a 0.3% year-on-year increase. Looking back, this volume level is 6.1% above the long-term average seen between 2001-2019, reinforcing the growing role used cars continue to play in a market shaped by ongoing cost of living pressures.

The upside scenario assumes dealer and consumer confidence remains resilient despite ongoing pressures, allowing the market to absorb higher stock flow without significant value disruption. In this outlook, volumes could rise to 8,026,607 units, a 2.8% year-on-year increase, and would be the market’s first return to 8-million units since the pandemic.

Meanwhile, the downside scenario is impacted by ongoing affordability concerns and competitive pressure and demand is eroded further than expected. Volumes fall to 7,234,099 units, which would be a 7.3% decline year-on-year, taking the market 1.9% below the 2001-2019 average.

Used Car Transactions Forecast 2026

Source: Cox Automotive

Upside scenario

In the upside case, the used‑car market remains a core profit and cash‑generation engine for retailers, with confidence and demand strong enough to absorb higher volumes without destabilising values. External pressures ease, and competitive disruption from new cars remains contained.

- Dealers continue to prioritise used cars as a key revenue stream, actively absorbing increased stock flow.

- Consumer confidence remains resilient, supporting steady demand across core used segments.

- Geopolitical pressures, including the Middle East conflict, have had a limited impact on used pricing or buyer behaviour.

- Increased new‑car competition has minimal knock‑on effect, with used buyers remaining value‑focused and price‑sensitive.

- Values stabilise, supporting healthy stock turn and margin protection.

Baseline scenario

In the baseline view, the used‑car market remains broadly stable, with volumes holding up but margins under pressure as retailers work harder to maintain throughput. Competitive new‑car activity creates some noise but does not materially disrupt used demand.

- Used volumes are tracking close to 2025 levels, with only a modest year‑on‑year uplift.

- Margin pressure persists as dealers balance pricing discipline with the need to sustain stock turn.

- Increased new‑car incentives create limited erosion at the margins, rather than a structural shift away from used.

- Consumer behaviour remains pragmatic, favouring affordability and availability over brand or fuel‑type shifts.

- The market continues to function efficiently, but without meaningful upside momentum.

Downside scenario

In the downside case, affordability pressures intensify, and new‑car pricing becomes aggressively competitive, pulling demand away from used vehicles and increasing volatility across pricing and margins.

- Heavy new‑car discounting and low entry offers drive meaningful erosion from used into new.

- Inflationary pressures re‑emerge, forcing base‑rate rises and weakening consumer and business confidence.

- Demand softens, extending days to sell and increasing stockholding risk.

- Used values come under downward pressure as supply outpaces demand.

- Dealer profitability is squeezed as price competition intensifies and margin recovery becomes harder to sustain.

To see the data behind the above forecast, please click here to view it in the Appendix.