IQ

Insight

Quarterly

Q1 | 2026

New market – Geopolitical tensions leave many questions to be answered for Europe’s outlook

Home

Home

The New Market

The New Market

The EV Market

The EV Market

The restructuring ripple: How slow EV adoption is reshaping automotive value chains

The restructuring ripple: How slow EV adoption is reshaping automotive value chains

The missing generation: How the pandemic stock gap is reshaping the UK used car market

The missing generation: How the pandemic stock gap is reshaping the UK used car market

Automotive advertising: changing habits for big gains

Automotive advertising: changing habits for big gains

The minefield just got more dangerous

The minefield just got more dangerous

Appendix

Appendix

Unpredictability on the global political stage has added further complexity to an already undulating new car market. Ongoing geopolitical tensions have heightened volatility across energy, commodities and logistics, amplifying cost pressures at every point of the value chain.

Against a backdrop of fragile consumer confidence and uneven global recovery, these external shocks have made short‑term market performance harder to interpret and long‑term planning more challenging for both manufacturers and retailers.

Reviewing Q1’s data, the picture is positive. While global new car sales softened in early 2026, down 2% year-on-year, driven mainly by a steep 34% drop in China, the UK new car market grew by 5.9% in Q1. Dealers are reporting pockets of strong volume and improved profitability.

However, this is tempered by emerging signs of strain, including localised losses in market share and increasing pressure on margins. In some cases, we have seen manufacturers resorting to guaranteed margins for retailers to mitigate against this somewhat.

Unfortunately, it is unlikely that this headline growth is structurally secure, as the UK faces a complex outlook for 2026, marked by rafts.

Much of the progress seen in the UK market comes from vehicles pre-registered earlier in the quarter, before the conflict broke out in the Middle East. The impact of this geopolitical volatility has caused significant energy instability globally. Brent crude has increased by 42% since the conflict began, pushing consumers to reconsider running costs. The UK has borne the brunt of this instability compared to the EU, largely due to its energy sourcing and exposure to rising oil and gas prices.

The FCA’s consumer car finance redress also threatens to further weaken already unstable consumer demand. The regulatory body’s final redress programme is likely to cause consumer caution, while lenders may exert a similar level of caution when offering private finance agreements. We have already seen early evidence of credit criteria and slower decision-making, which could dampen discretionary retail demand.

Overall, the results seen in the first quarter were as expected; however, the scale and composition are atypical as retail growth achieved was above the anticipated trend. As we move into Q2, the market is likely to be much less predictable, which may undermine the health that headline growth for the start of the year suggests. Consumer confidence remains highly sensitive to affordability pressures, energy prices and wider geopolitical uncertainty, all of which are likely to contribute to softening demand as Q2 progresses unless economic signals stabilise.

Looking for electric-specific insights? Head over to our electric market section for more information.

Short-term considerations

In the near term, we may see vehicle costs rise as a result of pressure on raw materials and shipping costs. Key commodities have been clearly impacted by geopolitical shifts, with lithium (+33%), cobalt (+13%) and nickel (+7%) all trending above January prices. This is further compounded by returning concerns over chip shortages, especially as new conflicts between Nexperia and its Chinese subsidiary are rumoured to be developing. This supply volatility may also impact stock availability.

Long-term implications

Looking further ahead, the risk of structurally higher costs driven by geopolitical instability is likely to persist. Prolonged trade fragmentation, alongside greater volatility in energy and raw material pricing, may continue to inflate vehicle production and distribution costs.

At the same time, increased import pressures, particularly from Chinese manufacturers with strong cost advantages and growing brand confidence, are reshaping competitive dynamics in the UK market. A recent consumer study commissioned by Cox Automotive revealed brand loyalty is undergoing a clear shift, with over 1 in 3 respondents (36%) saying their preference in manufacturers had changed somewhat in the last six months, with this figure jumping to 52% for those under 34.

While this may intensify pricing competition in certain segments, it also places greater strain on incumbent manufacturers and retailers who face rising input costs but limited scope to pass these on to increasingly price‑sensitive consumers.

Emerging dynamics

While affordability concerns may impact consumer demand, the pressure on oil and gas prices may push some demand away from traditional internal combustion drivers to hybrid and electric options. Octopus Energy reported a 27% increase in the sale of solar panels since the start of the Iran War as consumers looked to reduce their reliance on fossil fuels. While data in the automotive sector doesn’t reveal a notable shift in consumer behaviour, fuel price unpredictability may push consumers to consider alternative fuel types to mitigate against potential further instability.

What should the industry be keeping a close eye on this year?

The industry should be closely monitoring the ongoing impact of the Iran conflict on global supply chains and oil markets, which represents the most significant near‑term disruptor to cost stability. Sustained volatility in oil prices has direct implications not only for vehicle running costs and consumer demand, but also for manufacturing, logistics and dealer operating expenses.

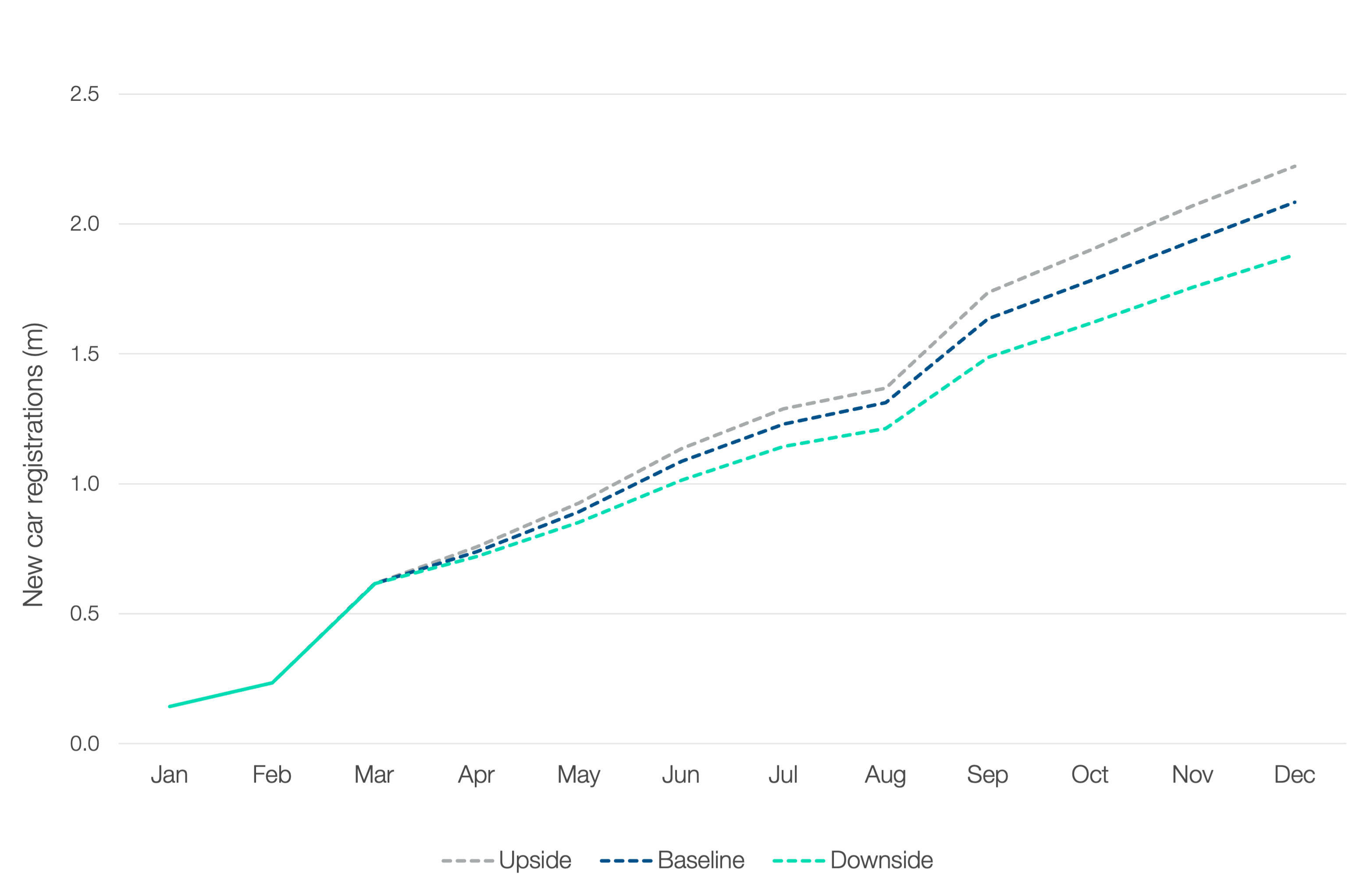

The new market: forecasts

Each quarter, we integrate proprietary market insight with the latest registration data to produce three 12-month outlooks: uplift, baseline and downside. These scenarios reflect differing macroeconomic, policy and industry assumptions, providing a structured framework to support stakeholder planning across a range of potential market outcomes.

This quarter’s forecasts reflect the increasingly volatile landscape the UK automotive faces, shaped by ongoing geopolitical uncertainty, increasing cost of living pressure and the continued expansion of new entrants, mostly from China, into Europe.

Our baseline scenario remains the most likely outcome, forecasting registrations to reach 2,082,665 units, representing a 3.1% year-on-year increase. Despite this growth, volumes would still sit 9.9% below the long-term 2000/2019 average, which underlines the structural reset of the market.

A more optimistic scenario with a supportive economic backdrop and sustained competitive momentum would see new entrants gain share and established brands respond more assertively. Under this scenario, registrations could rise to 2,222,587 units, equating to a 10% increase on 2025 and moving the market closer to pre-pandemic highs. Conversely, the downside scenario anticipates that geopolitical instability has a greater impact on inflation, interest rates and consumer demand. This scenario would see registrations drop to 1,881,043.

New Car Registrations Forecast 2026

Source: Cox Automotive

Upside scenario

In the upside case, geopolitical risk unwinds faster than expected and macroeconomic conditions turn supportive, allowing underlying demand to surface more clearly. Growth becomes less incentive‑led and more confidence‑driven, supporting stronger‑than‑expected market performance.

- A swift end to the Middle East conflict removes cost and confidence headwinds, stabilising supply chains and energy prices.

New entrants continue to scale alongside established brands, expanding the overall market without materially eroding incumbent share. - Improved affordability drives some migration from used to new, supported by competitive entry pricing and lower running costs.

Inflation pressures ease, and base‑rate stabilisation or reductions lift private and fleet confidence. - Shorter ownership cycles accelerate replacement demand, sustaining higher registration volumes.

Baseline scenario

In the baseline view, geopolitical tensions are already influencing costs, pricing, and sentiment, but the UK’s new car market remains resilient enough to weather them. Demand remains tactically supported and broadly stable despite ongoing external pressures.

- First‑quarter resilience continues, with demand supported by fleet activity, incentives and plate‑change dynamics.

- Ongoing Middle East disruption feeds into fuel, logistics and confidence pressures, but without triggering a sharp demand contraction.

- Chinese OEMs maintain a strong strategic focus on the UK, masking softer natural demand through increased choice and competitive pricing.

- Inflation remains sticky but contained, with base rates held steady and consumer confidence cautious rather than retreating.

- Market growth remains volume‑led and incentive‑supported rather than fully demand‑driven.

Downside scenario

In the downside case, prolonged geopolitical instability feeds directly into inflation, interest rates and consumer behaviour, suppressing demand and weighing heavily on market performance.

- The extended Middle East conflict drives sustained economic uncertainty and higher energy‑related costs.

- Inflation pressures persist, prompting further base‑rate increases and tighter affordability conditions.

- Consumer confidence stalls, prolonging ownership cycles and delaying discretionary purchases.

- New‑entrant growth slows as competitive intensity rises and funding conditions tighten.

- Registrations weaken as margin pressure increases and reliance on incentives deepens.

To see the data behind the above forecast, please click here to view it in the Appendix.