Home

Home

The New Market

The New Market

The EV Market

The EV Market

The restructuring ripple: How slow EV adoption is reshaping automotive value chains

The restructuring ripple: How slow EV adoption is reshaping automotive value chains

The missing generation: How the pandemic stock gap is reshaping the UK used car market

The missing generation: How the pandemic stock gap is reshaping the UK used car market

Automotive advertising: changing habits for big gains

Automotive advertising: changing habits for big gains

The minefield just got more dangerous

The minefield just got more dangerous

Appendix

Appendix

Welcome to the latest edition of Cox Automotive’s Insight Quarterly, our Q1 2026 analysis of the forces shaping the UK and European automotive markets.

As ever, this report brings together data‑led insight and market intelligence from across the new, used and electric sectors, looking beyond headline performance to understand what is really driving change and what that means for the months ahead.

At first glance, the opening quarter of the year offers reasons for cautious optimism. New car registrations in the UK have grown, electric vehicle adoption has reached record levels and the used market continues to provide a degree of stability in an otherwise uncertain environment. Yet, as this quarter’s analysis makes clear, these encouraging signals mask a far more complex and fragile reality. Growth across all three markets is increasingly being shaped by external forces rather than underlying demand, with geopolitical tension, regulatory uncertainty and affordability pressures distorting normal market dynamics.

In the new car market, robust Q1 volumes owe much to tactical activity and fleet‑led demand, while the impact of energy volatility, rising input costs and tightening consumer finance conditions is only beginning to filter through. At the same time, electric vehicles continue to gain ground, but not without consequence. Oversupply, aggressive incentive strategies and intensifying competition, particularly at the more affordable end of the market, are placing renewed pressure on margins and residual values, raising important questions about the long‑term sustainability of today’s pace of adoption.

Against this backdrop, the used market remains a critical source of stability. While residual values have largely stabilised following the post‑pandemic correction, performance varies sharply by fuel type and age profile. Structural supply constraints, shaped by years of under‑production, continue to support demand in some segments, even as growing volumes of young EV stock introduce new complexity into pricing and risk management. As across the wider market, predictability is giving way to greater variance, reinforcing the need for disciplined, data‑led decision making.

Taken together, the message from this quarter is a familiar but increasingly important one. The automotive market no longer follows predictable, cyclical patterns. Success in this environment will depend less on chasing volume and more on navigating volatility with structured insights and data-led strategies. We hope this edition of Insight Quarterly helps provide the perspective and confidence needed to do just that.

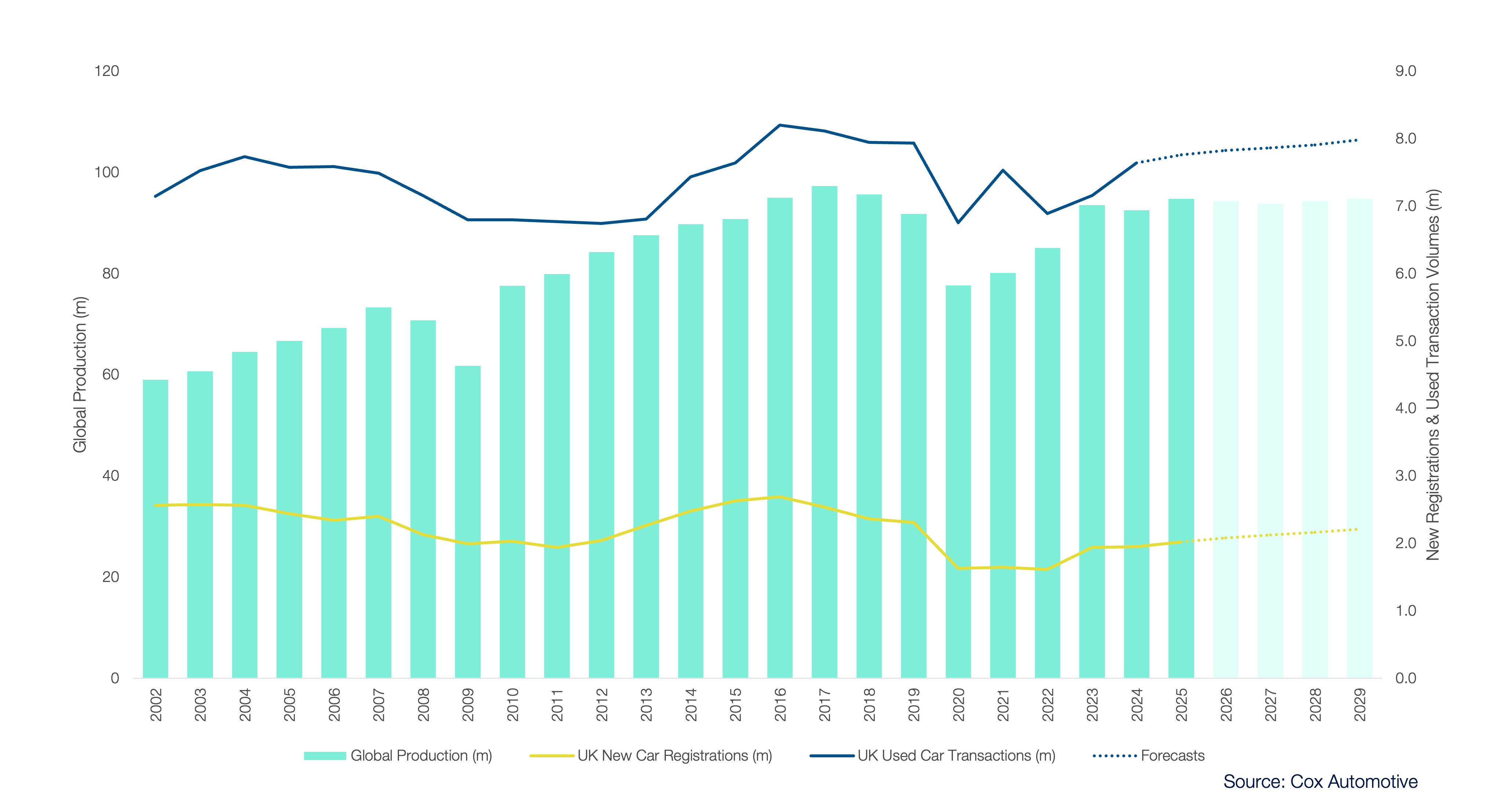

New & Used Sales vs Global Production Volumes