IQ

Insight

Quarterly

Q1 | 2026

The missing generation: How the pandemic stock gap is reshaping the UK used car market

Home

Home

The New Market

The New Market

The EV Market

The EV Market

The restructuring ripple: How slow EV adoption is reshaping automotive value chains

The restructuring ripple: How slow EV adoption is reshaping automotive value chains

The missing generation: How the pandemic stock gap is reshaping the UK used car market

The missing generation: How the pandemic stock gap is reshaping the UK used car market

Automotive advertising: changing habits for big gains

Automotive advertising: changing habits for big gains

The minefield just got more dangerous

The minefield just got more dangerous

Appendix

Appendix

The UK used car market has never had more stock – but the cars buyers want most are quietly running out.

Walk onto a used car forecourt in 2026 and there is no shortage of choice. Across the UK, Marketcheck UK is tracking over 900,000 unique used car listings every month, the highest level on record. Total stock has grown 13% since January 2024. By almost every headline measure, the market is in good health.

But look more closely at what those cars actually are, and a different picture emerges. The pandemic production gap, roughly 2.5 million cars that were never manufactured between 2020 and 2022 due to factory shutdowns and the global semiconductor shortage, is now working its way through the used market. Those missing vehicles would today be sitting in the 4 to 7 year age bracket, the segment that has historically driven the highest volumes and the strongest margins in used car retail. They are not there, and their absence is beginning to show.

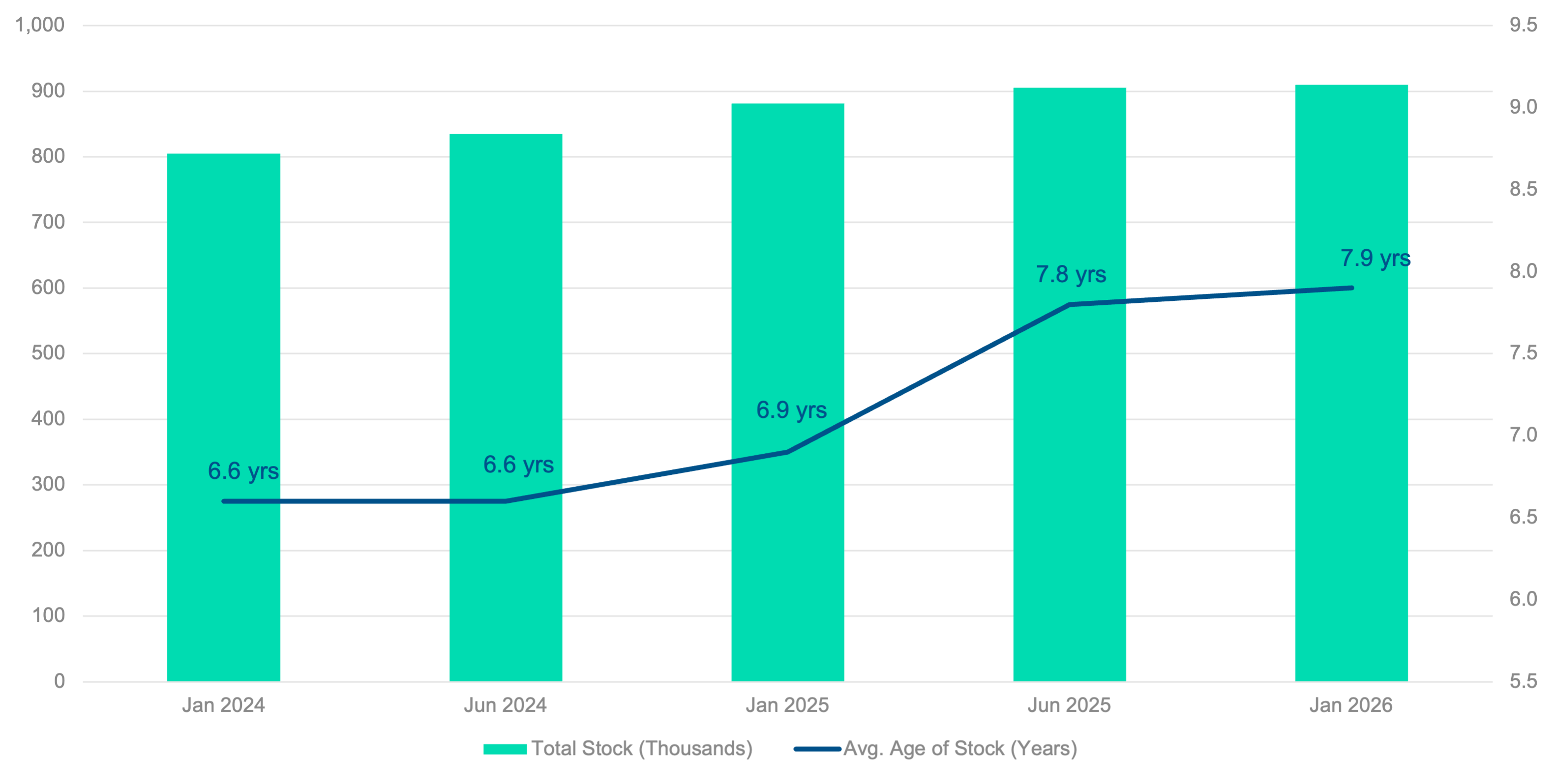

Stock Growing - But Getting Older

Source: Marketcheck UK — total stock listings and average age of stock, January 2024 to January

An ageing market

Marketcheck UK's data tracks every active used car listing across the country in real time. What that data shows is a market growing in volume but declining in the quality of what is available for the typical buyer. The average age of used car stock has risen from 6.6 years in January 2024 to 7.9 years by January 2026. That shift of nearly a year and a half in just two years is not a natural drift, it is the direct consequence of fewer newer vehicles entering the used pipeline.

For buyers, this means less choice in the age range where value is strongest. For dealers, it means increased competition for a shrinking pool of the most desirable stock. Independent retailers, who typically rely on second and third owner vehicles in the 5 to 7 year bracket, are likely to feel the pressure most acutely as 2026 progresses.

"The volume numbers flatter to deceive. Our data shows the market growing in listings but ageing rapidly. Dealers who rely on 5 to 7 year old stock are already operating in a tighter market than the headlines suggest, and that pressure will build through 2026 and beyond."

— Alastair Campbell, CEO, Marketcheck UK

Prices rising as choice narrows

When supply tightens in a segment that buyers want, prices respond. The average sold price across the used market has risen from £16,285 in January 2024 to £17,038 by January 2026, a rise of nearly 5% in two years. This is not general inflation at work. Broader consumer prices have remained relatively stable over the same period, and the overall volume of used car stock has grown. The price pressure is specific to the most desirable age bands, where competition among buyers is intensifying as supply shrinks.

This pattern echoes what happened in the immediate post-pandemic period, when production shutdowns caused a sharp reduction in nearly-new supply and prices across the used market hit historic highs. The current dynamic is more gradual, but it is driven by the same underlying mechanism: fewer of the right cars, more buyers looking for them.

Average Sold Price Rising as Desirable Stock Grows Scarcer

Source: Marketcheck UK — average used car sold price, January 2024 to January 2026

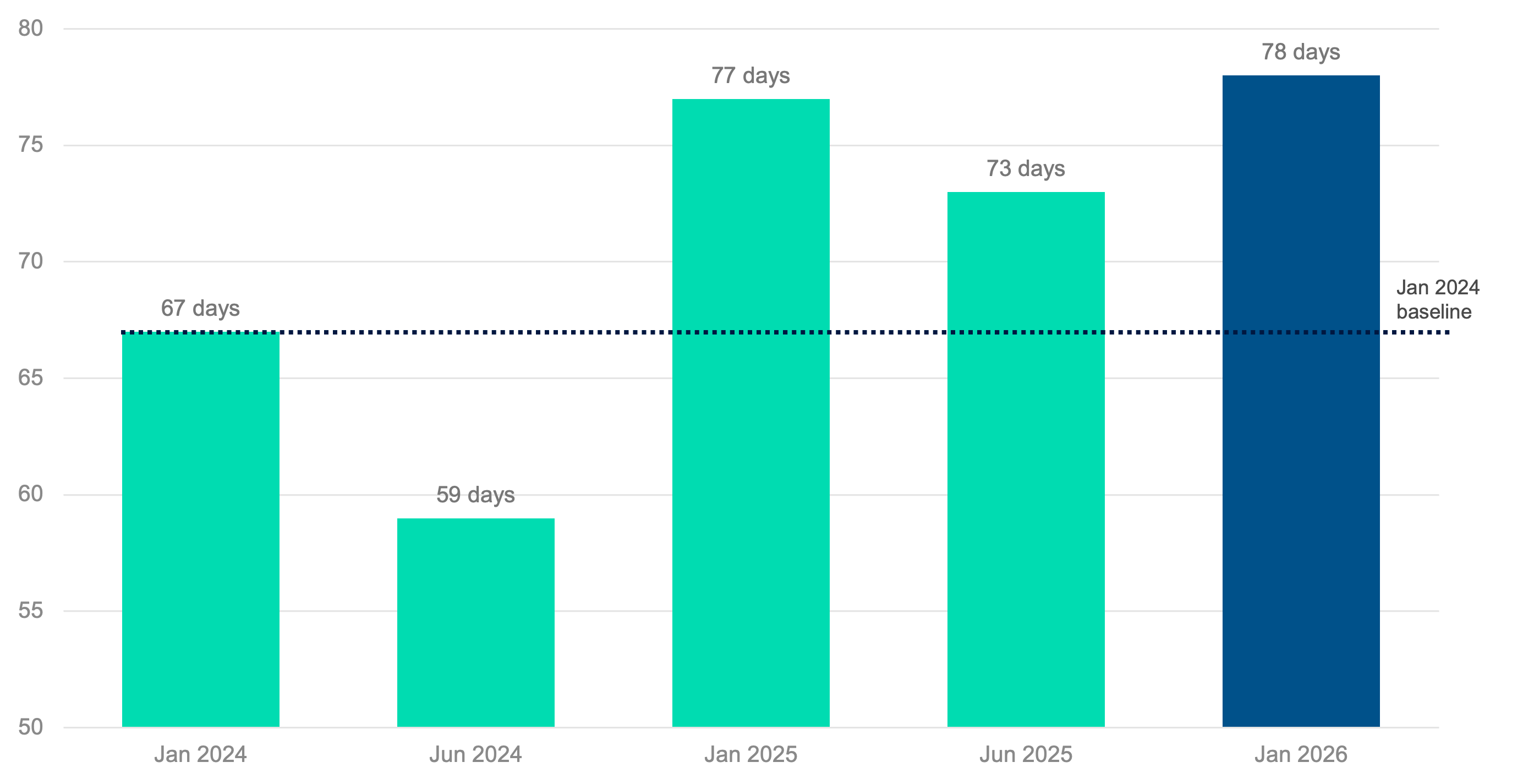

Buyers taking longer to find the right car

The third signal in the data is days on market. In January 2024 the average used car sold in 67 days. By January 2026 that has stretched to 78 days, a rise of 16%. On the surface this might suggest weaker demand, but the context matters. June 2024 saw the average fall to just 59 days, demonstrating that when the right stock is available at the right price, buyers move quickly. The subsequent rise reflects something different: buyers are not less willing to purchase, they are less able to find what they are looking for within a reasonable timeframe.

For finance providers, this widening period between listing and sale has practical implications for stock funding costs. For insurers, it affects how long vehicles sit exposed on dealer premises. For the broader market, it is a sign that the friction between available supply and active demand is growing.

Days on Market Stretching: Stock and Buyers Falling Out of Sync

Source: Marketcheck UK — average days on market (sold), January 2024 to January 2026

What this means for 2026 and beyond

The pressure is expected to intensify as the year progresses. Industry forecasters have warned that volumes of 5 to 6 year old vehicles could fall by as much as 25% to 30% during 2026 compared to 2024 levels, with further declines likely in 2027. Marketcheck UK's live data is already tracking the early stages of that shift in real time.

The market is not short of cars. It is short of the right ones. For dealers, lenders, insurers and investors, understanding that distinction, and acting on it ahead of the curve, will define who performs well in the months ahead.

Data source: Marketcheck UK proprietary listings database. All figures drawn from live and historical used car listing data tracking every active vehicle advert across the UK, January 2024 to January 2026.