Home

Home

Editor's Note

Editor's Note

The New Market

The New Market

The EV Market

The EV Market

What dynamics in the funding market tell us about the health of the used market?

What dynamics in the funding market tell us about the health of the used market?

What does 2026 hold for OEM manufacturers?

What does 2026 hold for OEM manufacturers?

A tale of two markets: UK used car buyers split between budget and luxury as middle ground shrinks

A tale of two markets: UK used car buyers split between budget and luxury as middle ground shrinks

Out with the old, in with the new

Out with the old, in with the new

Appendix

Appendix

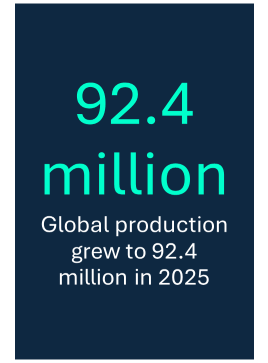

Based on headlines alone, you’d comfortably say that 2025 was a difficult year for automotive manufacturers. But a look under the bonnet at the S&P Global Mobility’s Global Light Vehicle production data might make you think otherwise.

Global production volume grew from 89.6 million vehicles in 2024 to 92.4 million in 2025, a 3.2% increase. While European volumes declined 1.5% to 16.9 million and by 1.3% to 15.2 million in North America, China had a stellar year with a 9.6% increase from 30.1 million in 2024 to just under 33 million in 2025. That’s quite a jump.

Only four or five years ago, China was starting to appear on the horizon for the automotive industry. Today, almost every conversation ultimately comes back to the influence that Chinese manufacturers now have on the global market. Many of the challenges facing legacy manufacturers in 2026 persist from the past 12 months, but three have amplified.

The global automotive market mix is experiencing a rebalance by brand and regional variations. In particular, the European manufacturers have seen declining sales in China in the past couple of years drive by an incredibly competitive market, excess capacity and rapid quality improvement of local brands. Quite simply, the European marques are being squeezed out, and it is hard to see that market share being regained any time soon.

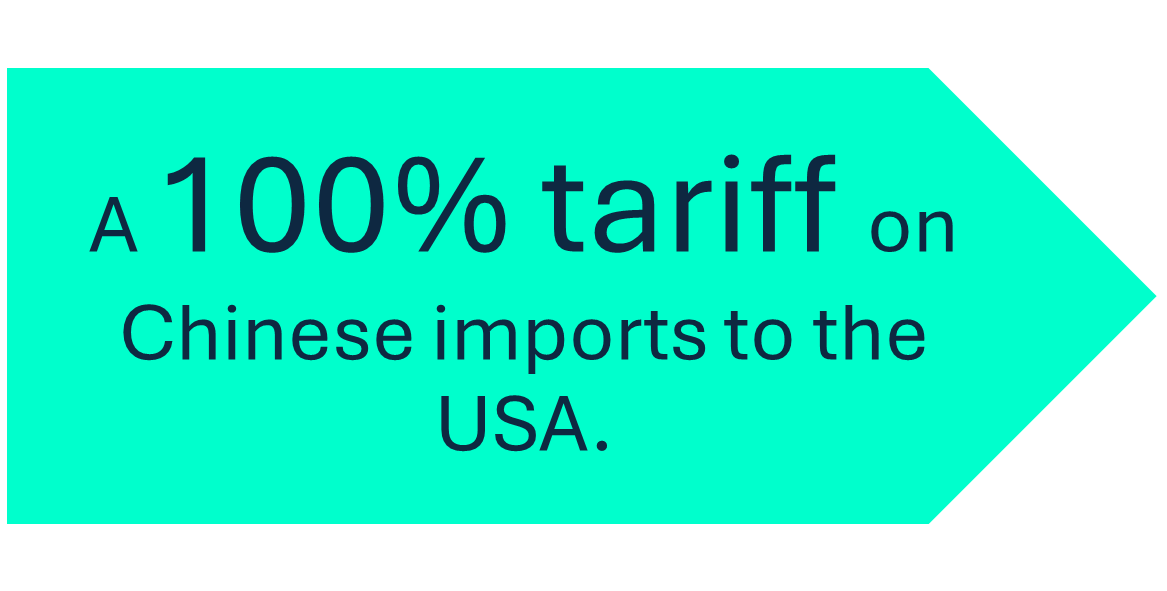

On the other hand, there’s China’s production boom, having achieved a 22% increase in vehicle volume to a peak of 33 million over the past six years. With a 100% tariff on Chinese imports to the USA, and with the same applying in Canada until only recently, Europe is in the spotlight alongside strong low-cost car markets targeted by China such as Mexico. At the centre of the Europe push is the UK due to its free market stance on tariffs.

Moving target

After the disruption caused by tariffs during 2025, rate agreements for the UK and EU were seen to have helped stabilise volatility. The first few weeks of 2026 have shown that geo-political uncertainty is far from settled. A lurch back to 100% tariffs for manufacturers exporting to the US would put a handbrake on trade.

EV transition marches on (just)

In the UK and Europe progress has been made in EV’s overall market share. However, it is fair to ask - how much of that is true customer demand versus product push from the OEMs to meet local emission targets?

The US has also lowered the emission standards from those set under the Biden administration and we have seen how manufacturers like Ford and GM have rowed back significantly on their EV plans as there’s little incentive in the US for companies to push EVs and little consumer appetite in a country wedded to the convenience of a petrol engine. In turn, those firms have taken large financial write-downs.

Meanwhile, the recent changes to emissions announced by the EU remain less than transparent and the UK government is undertaking a review of the Zero Emission Vehicle mandate. Of course, let’s not forget the Autumn Budget announcement to establish a pay per mile tax on EVs and plug-ins from 2028. While 3p per mile is significantly less than the equivalent taxes currently paid on petrol and diesel, it has potential to weigh down on future demand.

Tough decisions in the months ahead

The automotive sector is renowned for long lead times on programmes, which makes determining a way forward amongst such uncertainty a real task. Shortening cycle times is one way to meet that, as we’ve seen collaborations between OEMs to reduce lead times and costs, as well as new links in with Chinese manufacturers.

The three challenges I’ve outlined will be a challenge to address, but likely the most important that will determine success in years to come. No doubt 2026 will continue to have more twists and turns ahead. Let’s keep watching the geo-political situation and there will of course be winners and losers along the way. Bets made by OEMs three to four years ago may have to be reversed. I expect a more fleet-of-foot course will be the quality that sets leaders apart.