Home

Home

Editor's Note

Editor's Note

The New Market

The New Market

The EV Market

The EV Market

What dynamics in the funding market tell us about the health of the used market?

What dynamics in the funding market tell us about the health of the used market?

What does 2026 hold for OEM manufacturers?

What does 2026 hold for OEM manufacturers?

A tale of two markets: UK used car buyers split between budget and luxury as middle ground shrinks

A tale of two markets: UK used car buyers split between budget and luxury as middle ground shrinks

Out with the old, in with the new

Out with the old, in with the new

Appendix

Appendix

It’s a little late to be wishing readers a Happy New Year, but this is the first edition of Insight Quarterly for 2026, so it is probably a good point to reflect on what last year brought us, and what the priorities should be for the year just started. Will it be more of the same, or will the priorities and needs change?

Last year brought many uncertainties, affecting everyone in the automotive industry. Trump had barely settled into the Oval Office, before he started wreaking havoc with on-off tariffs that could have had a massive impact on the fortunes of the manufacturers – in the end, the main casualties were the ambitions of Chinese brands in the US and the long-established network of flows which had been created across the US, Canada and Mexico under NAFTA.

Trump, and others closer to home, slowed down or reversed the march towards electrification. War continued in Ukraine and paused in Gaza, with tensions remaining high, and a new focus on upping defence spending across Europe, drawing Government spending away from other areas that may help our industry.

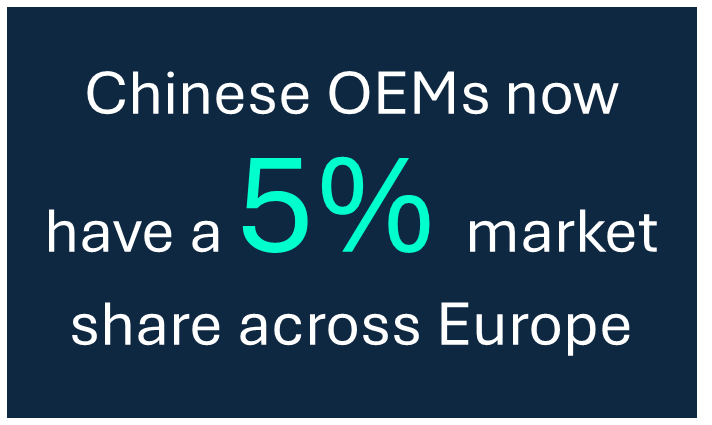

The onslaught by the Chinese OEMs stepped up, winning them a 5% market share across Europe, with many new brands arriving in multiple markets. It was therefore not surprising that caution was the common behaviour, seasoned with a need for agility. Most businesses in our sector seem to have weathered the storm reasonably well, even if some, like Porsche, took a major financial hit that they hope will have cleared the decks.

As many of the drivers of uncertainty in 2025 remain in place for 2026, it is difficult to see why the strategic landscape will change significantly, but businesses cannot stay in a holding pattern forever. A business that is not moving forward is inevitably actually slipping backwards.

There is no easy answer to how you deal with on-off tariffs as a manufacturer, but it certainly feels like globalisation and free trade has taken a step back for the long term, not just under Trump’s presidency. That will affect the manufacturing footprint of both established and new manufacturers, and in principle increase product costs as sub-optimal decisions are made on sourcing and how manufacturing capital investment is replicated in multiple locations. In the near term, this will erode some of the Chinese product cost advantage, even if they save on tariffs, and may therefore affect their ability to be as competitive in the market.

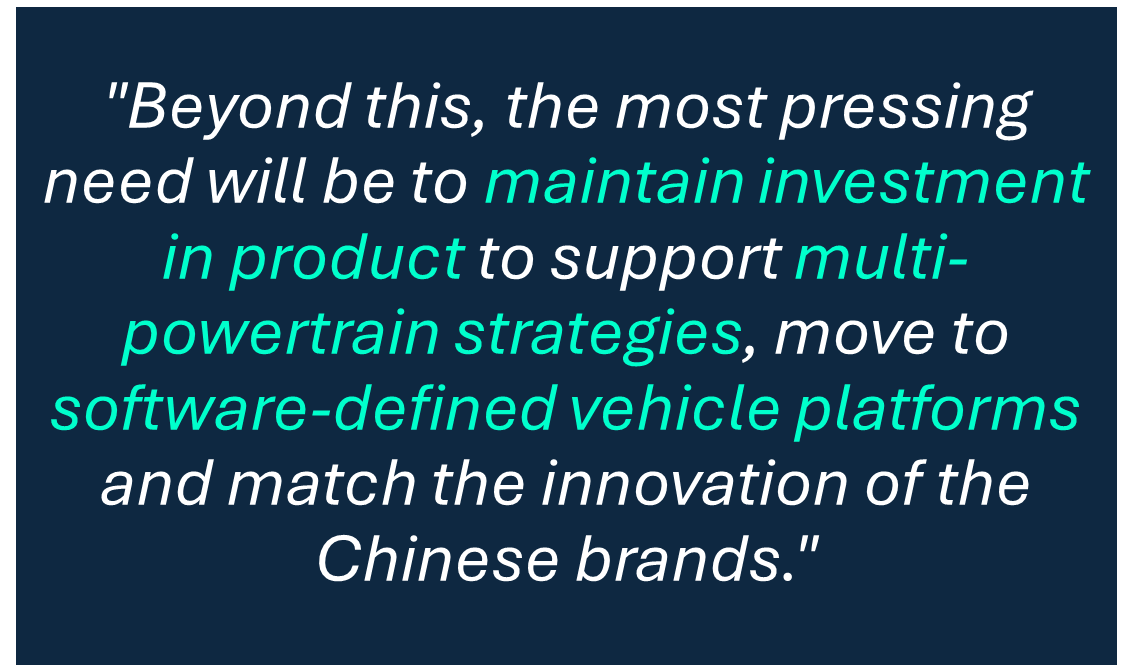

Beyond this, the most pressing need will be to maintain investment in product to support multi-powertrain strategies, move to software-defined vehicle platforms and match the innovation of the Chinese brands. Network strategies will see evolutionary rather than revolutionary change.

Most dealers were heavily focused on costs in 2025, with dealership closures and staff redundancies.

Given that the economic outlook is for set to see very slow improvement (although always subject to upset if any of the current global hotspots flares up), dealers can hopefully draw a line under that process and get back to business improvement, optimising their OEM brand representation across their brand portfolio, investing in their people and technology, including AI, and pushing for a balanced contribution from the three critical areas of new and used sales and aftersales. They will still have to deal with the consequences of on-off electrification and the pressures and opportunities from the new entrants, but it will feel more like ‘business as usual’.

For other players – providing technology and services to the OEMs, dealers, repairers, other direct operators and not least the end customers – the difference between success and disappointment will be whether you back more winners than losers. In such a period of change, there must be mixed fortunes ahead, but as a provider to the sector, you have the opportunity to manage your risk by working with a broad client portfolio. Take advantage of this and adjust resource allocation as new information emerges on where the returns are likely to do better.

Good luck for 2026!