Chinese EV brands: What UK consumers really think about the new wave of car makers

The UK automotive market has changed dramatically over the past decade. New brands have entered at a pace not seen for many years, bringing fresh competition, new technologies and different approaches to vehicle design and ownership.

At the centre of this shift are Chinese EV brands. Once largely unknown to UK consumers, manufacturers such as BYD, MG, OMODA, JAECOO, XPENG and Leapmotor are becoming increasingly visible on UK roads and showroom forecourts.

Their arrival comes at a time when consumer priorities are evolving. Affordability remains a key concern for many households, while demand for electric vehicles continues to grow. At the same time, buyers are becoming more willing to explore alternatives to traditional automotive brands.

Yet despite their rapid growth, consumer attitudes towards Chinese electric vehicles remain far from settled. While some drivers are attracted by competitive pricing, advanced technology and generous warranties, others remain cautious about quality, reliability and long-term ownership.

Using consumer research conducted by Cox Automotive, this article explores what UK consumers really think about Chinese EV brands, what is driving interest in these challenger manufacturers, and what barriers still stand in the way of wider adoption.

Why are Chinese EV brands gaining momentum in the UK?

The rise of Chinese EV brands reflects broader changes taking place across the global automotive industry.

China has become one of the world's largest automotive manufacturing centres, with many manufacturers benefiting from significant scale and extensive investment in electric vehicle technology. As competition intensifies in their home market, many of these manufacturers have turned their attention to Europe, and the UK has become one of the most important markets in that expansion.

The UK is now home to more than 75 automotive brands, making it one of the most competitive vehicle markets in Europe. New market entrants accounted for 9.83% of registrations in January 2026, up from just 2.65% in January 2025.

For consumers, this increased competition brings greater choice. For established manufacturers, it creates fresh pressure to differentiate their products and maintain market share.

Many of the new Chinese electric car brands entering the UK have positioned themselves around three core strengths:

- Competitive pricing

- Advanced technology

- Comprehensive ownership packages

Combined, these factors have helped challenger brands attract attention in a market that is becoming increasingly open to alternatives.

Are UK consumers open to buying a Chinese electric car?

While headlines often suggest a wholesale shift towards new manufacturers, the reality is more nuanced. Consumer attitudes are clearly changing, but widespread adoption is far from guaranteed.

Research conducted by Cox Automotive found that more than a third of UK drivers (36%) said their preference for vehicle manufacturers had changed somewhat during the previous six months. This suggests that many consumers are actively reassessing the brands they would consider for their next vehicle purchase.

However, willingness to change manufacturers does not necessarily translate into willingness to buy from one of the new challenger brands. Among drivers who do not currently own a vehicle from a new market entrant, only 15% said they would consider one for their next purchase.

This highlights an important distinction: Chinese EV brands have captured the attention of UK consumers, but convincing them to make the purchase remains a challenge, for now.

Some established manufacturers appear more exposed than others. In our research, drivers of German brands were the most likely to express interest in a challenger brand, with 20% saying they would consider making the switch. By comparison, only 11% of drivers of British and American brands expressed the same level of interest.

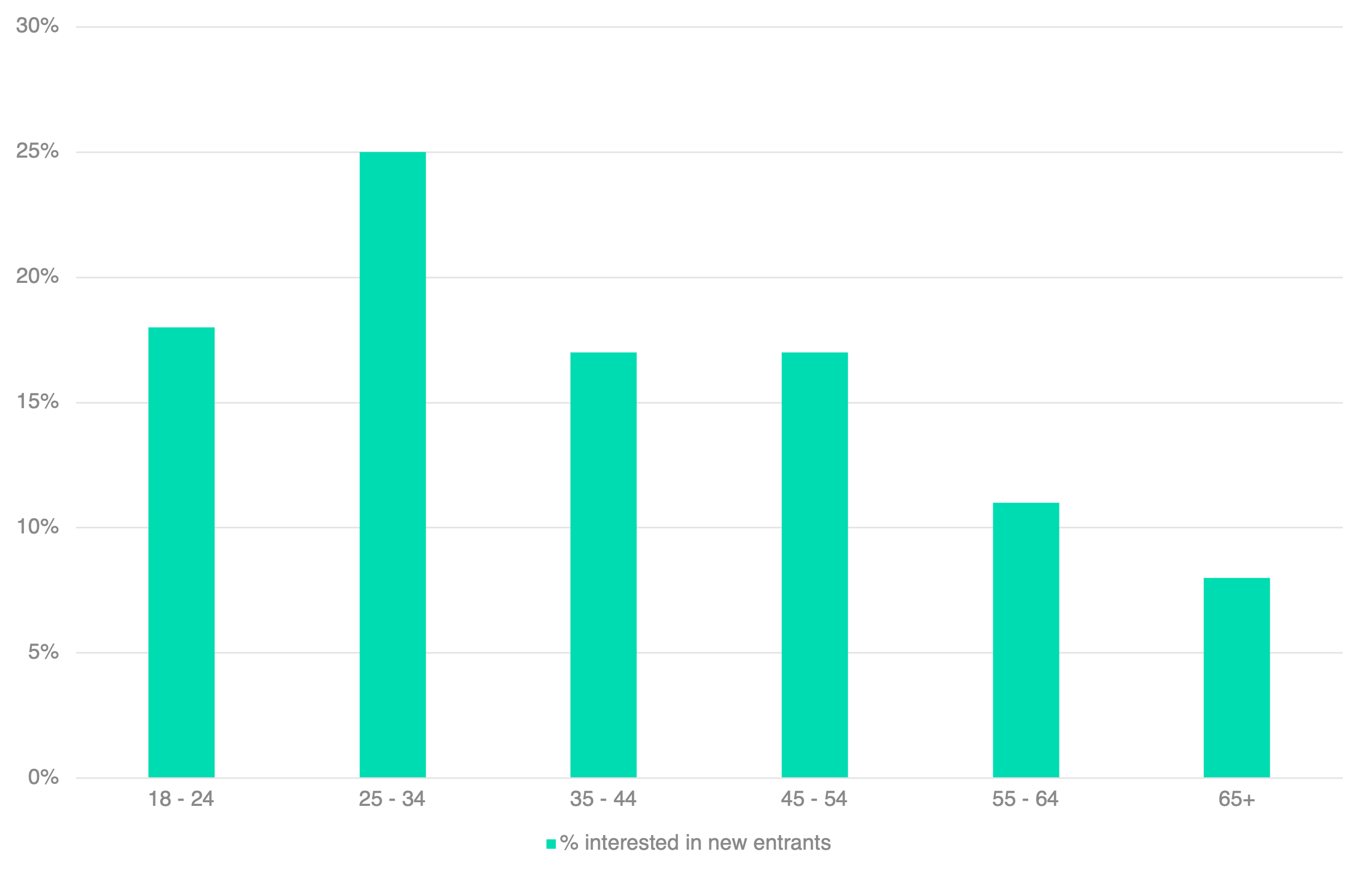

Younger drivers are leading the shift

One of the clearest findings from the research is the generational divide in attitudes towards challenger brands. Younger drivers appear significantly more willing to explore alternatives to established manufacturers.

A quarter of drivers aged between 25 and 34 said they would consider purchasing a vehicle from a new market entrant, compared with just 11% of drivers aged 55 to 64.

Younger consumers also showed much lower levels of brand loyalty. More than half of respondents under the age of 34 reported changing their manufacturer preferences during the previous six months, while only 16% of drivers aged 55 to 64 said the same.

For newer manufacturers, this presents a significant opportunity. Consumers who have fewer long-standing brand attachments are often more willing to assess vehicles based on features, technology and value rather than heritage alone.

Regional attitudes tell a different story

Attitudes towards Chinese EV brands also vary considerably across the country.

Drivers in Southeast England displayed some of the highest levels of confidence in purchasing from a new market entrant, while confidence was lower across parts of Northern England and the Southwest.

London drivers were among the most receptive, with nearly half expressing confidence in purchasing from a new brand. Meanwhile, Scotland demonstrated a particularly mixed picture, with confidence levels differing significantly between Glasgow and Edinburgh.

These regional differences suggest that local market conditions, consumer demographics and levels of exposure to new brands may all influence purchasing attitudes.

What attracts buyers to Chinese EV brands?

Much of the discussion around Chinese electric vehicles focuses on pricing, but the research suggests consumers see value in other areas too.

When asked what would encourage them to consider a new market entrant, respondents identified several factors:

Affordability remains the strongest advantage

The most frequently cited reason was value for money. A third of respondents said a lower purchase price and stronger overall value proposition would encourage them to consider a challenger brand. A further 31% highlighted lower running costs as a key attraction.

This reflects the financial pressures many consumers continue to face and reinforces the importance of affordability in the transition to electric vehicles. For many buyers, Chinese EV brands are helping make EV ownership feel more accessible.

Technology is attracting attention

Technology is helping sustain consumer interest in additional to attractive pricing,

More than a quarter of respondents identified better EV range or technology as a reason they would consider a challenger brand. This was particularly evident among younger drivers, who were more likely to be influenced by technology, connected features and the overall in-car experience.

Many Chinese EV manufacturers have built their products around digital-first experiences, often incorporating large infotainment displays, advanced driver assistance systems and over-the-air software updates as standard features. As vehicles become increasingly software-defined, this emphasis on technology is proving attractive to a growing segment of the market.

Longer warranties help build confidence

Trust remains a major hurdle for any new automotive brand, and one way many Chinese manufacturers are addressing this challenge is through extended warranty coverage.

A quarter of respondents said longer warranties would encourage them to consider a new entrant brand. For consumers, these warranties can help reduce concerns around reliability and long-term ownership costs. For manufacturers, they provide an opportunity to demonstrate confidence in their products while building credibility in unfamiliar markets.

What concerns do consumers still have about Chinese EV brands?

Despite growing interest, significant barriers remain. The research found that only 35% of consumers would feel confident purchasing a vehicle from a new market entrant brand, leaving two-thirds that need to be convinced.

Quality concerns remain the biggest obstacle

Vehicle quality was the most commonly cited concern among respondents, with more than half of drivers identifying it as a barrier to purchasing from a challenger brand.

This reflects the reality that reputation takes time to build. While many Chinese manufacturers have invested heavily in engineering, manufacturing processes and product development, consumer perceptions often lag behind. For many buyers, confidence comes from years of brand familiarity and positive ownership experiences, and new entrants must earn that trust.

Reliability of technology remains under scrutiny

Technology may be a key attraction for many, but it is also a source of concern for the rest. Half of respondents expressed reservations about the reliability of the technology offered by challenger brands.

Interestingly, concerns about technology reliability were relatively consistent across age groups, suggesting that even digitally confident consumers still want reassurance that systems will perform reliably over the long term.

Aftersales support matters

Buying a vehicle is only the beginning of the ownership journey. Access to servicing, maintenance and repairs remains an important consideration, yet for more than a third of respondents, access to service partners was cited as a concern when considering a new market entrant.

This is an area where established manufacturers often benefit from decades of investment in dealer networks and aftersales infrastructure. While many Chinese EV brands are rapidly expanding their retail and service networks, consumers still need confidence that support will be available throughout the life of the vehicle.

Questions around resale value persist

Unsurprisingly, resale value was another significant concern, cited by 34% of respondents. Residual values are influenced by brand perception, used vehicle demand and long-term market confidence.

While this reflects a wider concern around EV residual values that the market is addressing, for newer brands with limited historical data, this effect can be amplified.

As more Chinese EVs enter the used vehicle market over the coming years, the industry will gain a clearer understanding of how these vehicles perform from a residual value perspective.

How are established manufacturers responding?

One of the more interesting findings from the research is what is not driving consumers towards challenger brands.

Only 4% of respondents said dissatisfaction with traditional manufacturers was influencing their interest in new entrants, suggesting that established brands are not necessarily losing customers because they are failing. Instead, consumers are being attracted by the strengths that challenger brands bring to the market.

It appears that competition is increasingly centred on value, technology, ownership experience and innovation rather than simple brand loyalty. As Chinese EV brands continue to gain visibility, established manufacturers may need to place greater emphasis on demonstrating their own strengths, whether through quality, heritage, aftersales support, product differentiation or customer experience.

Ultimately, the arrival of challenger brands is raising expectations across the industry.

What does the future hold for Chinese EV brands in the UK?

Chinese EV brands are becoming an increasingly influential force in the UK automotive market. Their combination of competitive pricing, advanced technology and attractive ownership propositions has helped them capture the attention of consumers and challenge established manufacturers.

However, the research shows that interest alone is not enough. Concerns around quality, technology reliability, servicing support and resale values continue to shape consumer decision-making.

For many buyers, the question is no longer whether Chinese EV brands deserve consideration. Instead, it is whether these manufacturers can build the trust needed to compete alongside long-established automotive names.

Awareness of Chinese EV brands is growing rapidly, and more vehicles are entering both the new and used vehicle markets. Cox Automotive estimates that up to 67,000 vehicles from the six leading new market entrants could enter the used parc during 2026 alone.

As those vehicles move through their ownership cycles, consumers will gain a clearer understanding of their real-world quality, reliability and long-term value.

For more EV market insights and data, visit our EV Hub.

2026 UK EV adoption and perceptions report

Our 2,000+ UK driver survey shows how experience is driving EV confidence and shifting purchase intent.

EV trends 2026 – Industry predictions shaping the future of electric vehicles

From policy shifts to pricing pressures and sustainable scalability, discover the EV trends 2026 shaping electrification across the UK and Europe.