A joint report between Cox Automotive and Grant Thornton has revealed the true extent of manufacture-related disruption within the automotive retail market throughout the Coronavirus pandemic and shines a light on individual recovery strategies.

Data revealed by the two businesses shows significant losses affecting all major manufacturers in the early stages of the pandemic, since March 2020, with Chinese manufacturers unsurprisingly suffering the earliest hit due to plant closures, closely followed by the rest of Europe. However, the report also gives cause for confidence, with evidence that major manufacturers such as Tesla, General Motors, Kia and Toyota still managed to make a profit in Q2 of 2020 and rebounded quickly to growth halfway through the pandemic.

With factories closed and the retailing of vehicles also on hold, there was little OEMs could do to stop their profits from being impacted in the early stages of the pandemic. As a result, cost reductions where possible were quickly put into place and staff put on furlough where possible.

Recovery tactics

One OEM that comes out of the report favourably is Tesla, which was able to hold onto profit for a substantial length of time by diverting manufacturing to China as the country shook off the worst of the pandemic before it spread across Europe.

Owen Edwards, Associate Director at Grant Thornton UK LLP, who wrote the report, explained: "Tesla continued to make profits, delaying the closure of production in its Fremont plant in the US, for as long as possible and reopening production as quickly as possible when it could. Where and when possible, some production was diverted to China.

"However, the normalised numbers need to be reviewed carefully as Tesla continued to benefit from both the strong rebound in the market and from other OEMs purchasing Regulatory Credits (also known as environmental credits). Therefore, removing the income from Regulatory Credits to leave only income generated from the production of vehicles meant that the business was in loss throughout Q1 and Q2 2020. Vehicles produced nevertheless continued to increase, and it was not until Q3 that Tesla's normalised EBIT ex Regulatory Credits started to make profits."

The report also shows that OEMs responded quickly to the change in the market by making cost reductions. For example, despite having made losses in Q2 2020 of US$6.1bn, Ford's performance improved in Q3 with a solid rebound to US$2.8bn profit caused by its focus on high-value vehicles such as SUVs and pickup trucks, which enjoyed a substantial increase in demand after the pandemic's initial impact. Furthermore, Ford's cost reduction plan, which started in 2017/18, realised value.

Stellantis also experienced a strong rebound from a US$0.96bn loss to US$2.2bn profits in Q3 2020. In addition, Stellantis benefited from continued cost reductions from its recent acquisitions of Opel/Vauxhall and FCA.

However, Nissan Motor Company was heavily affected by the lack of production in Q1 and Q2 2020, making significant losses of US$94bn and US$153bn, respectively. Nissan was already struggling in the US market before the pandemic, and this was compounded by the drop in production over Q1 and Q2 2020. Nevertheless, the cost reductions meant that the business generated less severe losses than investors had expected. Further cost-cutting took place over the period, and vehicle volumes returned; by Q3 2020, Nissan was making a profit.

Honda and Mazda both followed a similar trend, with Honda becoming profitable in Q3 2020 and Mazda following in Q4 2020.

As 2020 ended and Q1 2021 began, most of the OEMs were generating profits, with the exception of Nissan.

Philip Nothard, Insight and Strategy Director for Cox Automotive, shared details of the report in the latest issue of AutoFocus, in which he explains what all of this means for the burgeoning used vehicle market.

"What these findings demonstrate is that the new vehicle market is not all doom and gloom, and manufacturers have done extraordinarily well to bounce back their fortunes with some using highly creative methods. While there is no doubt that current well-publicised material shortages are causing a slowdown in the new vehicle market and impacting on used supply and demand, manufacturers have demonstrated that they can be agile and adaptable enough to ride these situations out, which offers some hope for future recovery."

Coil roll steel price increases

Speaking about how 2021 is expected to end, Edwards added: "It is difficult to say; after a strong performance in Q1 2021, there are further headwinds to navigate. For example, there is increasing evidence of supply chain issues, shortages of raw materials and high raw material prices, which could affect the price and supply of new vehicles. Meanwhile, the demand for hot-rolled coil steel used in the automotive industry for chassis has increased significantly in 2021.

"However, automotive OEMs have reasons to be optimistic about the short-term outlook. They are resistant to disruption and adversity, and demand for vehicles is still robust. This can be attributed to the way vehicles are sold, through structured finance products.

"We've enjoyed a prolonged period of low-interest rates, making borrowing affordable. Demand is expected to continue this year, but clearly questions remain around the short supply of vehicles. With vehicle shortages profit margins for both the new and used car markets are expected to remain high."

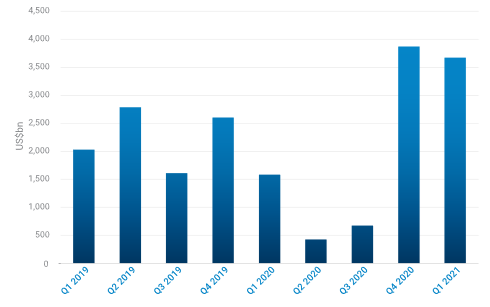

Image extracted from the report: combined OEM normalised EBIT from Q1 2019 to Q1 2020, sourced from Thomson Reuter and company websites